Article Text

Abstract

Mexico is the largest soft drink market in the world, with high rates of obesity and type 2 diabetes. Due to strains on the nation’s productivity and healthcare spending, Mexican lawmakers implemented one of the world’s first public health taxes on sugar-sweetened beverages (SSBs) in 2014. Because Mexico’s tax was designed to reduce SSB consumption, it faced strong opposition from transnational food and beverage corporations. We analysed previously secret internal industry documents from major corporations in the University of California San Francisco’s Food Industry Documents Archive that shed light on the industry response to the Mexican soda tax. We also reviewed all available studies of the Mexican soda tax’s effectiveness, contrasting the results of industry-funded and non-industry-funded studies. We found that food and beverage industry trade organisations and front groups paid scientists to produce research suggesting that the tax failed to achieve health benefits while harming the economy. These results were disseminated before non-industry-funded studies could be finalized in peer review. Mexico still provided a real-world context for the first independent peer-reviewed studies documenting the effectiveness of soda taxation—studies that were ultimately promoted by the global health community. We conclude that the case of the Mexican soda tax shows that industry resistance can persist well after new policies have become law as vested interests seek to roll back legislation, and to stall or prevent policy diffusion. It also underscores the decisive role that conflict-of-interest-free, peer-reviewed research can play in implementing health policy innovations.

- diabetes

- health policy

- nutrition

- public health

Data availability statement

Data are available in a public, open access repository.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Summary box

Food and beverage industry opposition can intensify after a soda tax has been enacted because vested interests hope to weaken or delay implementation, and prevent policy diffusion to other countries.

After the Mexican soda tax took effect in 2014, transnational food and beverage corporations recruited scientists to produce credible-seeming evidence that the policy was failing to achieve its goal of reducing sugar-sweetened beverage (SSB) consumption.

Industry-funded studies were rapidly disseminated and amplified outside the scientific literature in international news outlets and global health policy discussions to argue that the tax was failing to achieve its goal of reducing SSB consumption.

Mexico ultimately played a decisive role in garnering international attention on soda taxes by providing the first real-world context for peer-reviewed studies documenting their effectiveness.

Introduction

Mexico is the largest soft drink market in the world, with average consumption at 151 L per capita per year.1 The country also has disproportionately high rates of obesity and type 2 diabetes.2 Due to strains on the nation’s productivity and healthcare spending, Mexican lawmakers implemented one of the world’s first public health taxes on sugar-sweetened beverages (SSBs) on 1 January 2014 as part of its federal budget.3 At the time, a few developed countries with low consumption rates had soda taxes (eg, France, Finland),4 but there was no empirical research on their effectiveness, only price-elasticity simulations based on alcohol and tobacco taxation. These simulations suggested that a 10% increase in the price of SSBs was associated with an 11% decrease in consumption.5 6

Since Mexico implemented its tax, soda taxation has become an international movement.7 Thirty-five countries around the globe have adopted SSB taxation policies, including Chile, India, and the UK.4 8 Three systematic reviews now conclude that taxation is effective for reducing SSB consumption,9–11 with the first empirical studies based on Mexico.12–17

Because they are designed to reduce SSB consumption, soda tax proposals and related public health strategies (eg, warning labels and SSB sales bans in schools) have routinely faced opposition by transnational food and beverage corporations in Mexico and globally.18 19 A key opposition strategy is to fund scientists to produce evidence favourable to industry interests.18 20 While industry opposition during debates over passage of the Mexican soda tax has already been documented,19 21–24 little is known about the industry’s tactics after the policy took effect.

We reviewed and organised in chronological order previously secret internal industry documents contained in the University of California San Francisco’s Food Industry Documents Archive25 to investigate the industry’s reponse to implementation of Mexico’s tax both within Mexico and in international context (online supplemental table 1). This publicly available repository contains internal memos, emails and other private communications between executives from leading transnational beverage corporations, such as Coca-Cola, and the researchers they fund. These documents, many obtained through litigation and under freedom-of-information laws, provide a window into the behind-the-scenes motives, interests and strategies of transnational food and beverage corporations that resist regulations, such as soda taxes, designed to reduce consumption of ultra-processed foods and beverages at the population level. We also used standard qualitative analysis methods, guided by the policy dystopia model,26 27 to review all available research reports on evaluations of the effectiveness of Mexico’s tax policy. Here, we compared the results reported by industry-funded and non-industry-funded studies to better understand the role of science in this debate. (See online supplemental data for details on document sources and research methods.)

Supplemental material

The food and beverage industry’s response to Mexico’s implementation of a soda tax

During 2014, Mexico’s Health Minister, Mercedes Juan, who formerly directed a Nestlé-funded research organisation, created the Mexican Observatory on Non-communicable Diseases (OMENT) to monitor obesity and diabetes, including the effects of the soda tax.28 Juan appointed an Advisory Council with representatives tied to the food and beverage industry,21 29 including key trade groups that had opposed passage of the tax, arguing that it would harm the economy.

In June 2015, Mexican government scientists reported that nationwide, SSB purchases appeared to have gone down by 6% because of the tax.30 In July, the National Alliance of Small Merchants (ANPEC) gave a press conference to present data suggesting that 30 000 small stores had been forced to close down due to the tax.31 Shortly thereafter, the National Association of Soda and Carbonated Water Producers (ANPRAC) released a study claiming that the tax was regressive because it negatively impacted Mexicans with low purchasing capacity.32 Soon came another industry-funded study reporting that SSB sales had decreased by 3%–4.4%, amounting to a negligible reduction in daily calories for the average Mexican, while producing 10 815 job losses.33 Industry-funded researchers at the Mexican Autonomous Institute of Technology (ITAM) released yet another study concluding that, while SSB purchases had decreased by 6.5%, total calories were reduced by only 1%, with no impact on obesity.34 (See online supplemental table 2 for details on all studies.)

In late 2015, Coca-Cola and its Mexican bottlers began lobbying for reductions in the tax on lower-sugar beverages to create ‘an incentive based on the reduction of the caloric content to effectively impact the fight against obesity’.35 The idea appeared in recommendations by the Finance Commission of the Chamber of Deputies for the 2016 federal budget.36 37

In September 2015, 1 month prior to the federal budget vote, the Mexican Branch of the International Life Sciences Institute (ILSI Mexico), a Coca-Cola-funded scientific front group at the time,38 sponsored the national symposium, Sweeteners and Health. Cosponsoring was the Rippe Lifestyle Institute of Shrewsbury, Massachusetts, USA, a centre providing research services to beverage corporations, including Coca-Cola and PepsiCo.39 In a series of private emails, its founder, Dr James Rippe, networked with other US academics to recruit scientists to present research at the symposium, promising ‘a modest honorarium if you decide to turn your presentation into one of the ASN (American Society for Nutrition) journals or another academic journal’.40 Rippe noted that ‘the symposium comes at a very important time in Mexico and relates to a number of issues that are very important in this country’.40 Speakers at the symposium argued that ‘sugar is not the enemy, the problem is calories’,41 and questioned whether Mexico was ‘taxing the right food group, if their intention is to curb obesity’.42 In the plenary session, Rippe stated that ‘taxing SSBs will not reduce consumption, and will not do anything meaningful for obesity and diabetes’.43 During the symposium, a report was circulated claiming that even with a much-larger tax of 20%–40%, ‘the impact on BMI (body mass index) would be marginal’.44

The symposium drew negative press for ILSI Mexico,45 including criticisms that international scientists had been recruited to ‘fight the tax’.45 46 ILSI International ultimately suspended ILSI Mexico ‘for engaging in activities that can be construed to be policy advocacy and/or public relations efforts to influence policy’.47 In a private email, Alex Malaspina, former Coca-Cola executive and Director of ILSI International, wrote to a Coca-Cola-funded scientist at the University of Colorado, Dr James Hill, about ‘the mess ILSI Mexico is in because they sponsored in September a sweeteners conference when the subject of soft drinks taxation was discussed … A real mess’.48

The proposal to reduce the Mexican soda tax ultimately passed in the Chamber of Deputies49 but failed in the Senate, leaving the original tax policy in place.50

In January 2016, the first peer-reviewed empirical study evaluating the Mexican soda tax appeared in BMJ.12 Industry stakeholders responded in March 2016 with another academic symposium featuring Mexican, American, and Canadian industry-funded scientists presenting findings that soda taxes fail to impact obesity.51 Months later, ANPRAC launched the website, calorictaxes.com, to disseminate industry-funded research showing that the tax had failed to impact SSB consumption or obesity, while imposing significant economic hardships on the poor.52

The Mexican soda tax in international context

Our analysis of internal industry documents revealed that numerous Coca-Cola executives leveraged their global networks to disseminate the above-described industry-funded studies along with their key messages that the Mexican tax failed to lower SSB consumption and was harmful to the economy.53–58 In 2015, Coca-Cola International’s Manager of Public Affairs emailed some of these studies to executives in Communications and Government Relations as ‘relevant and useful updates on the excise tax in Mexico … (for) engaging stakeholders to demonstrate why excise taxes on our products are not effective policy mechanisms and can have unintended negative consequences, such as significant job losses’.59 Coca-Cola’s Vice President of Government Relations and Public Affairs further disseminated the studies to company executives on the Global Pacific leadership team, noting that, ‘After the call today, please find all of the latest materials to us in responding to the claims that the excise tax in Mexico has been effective’.59

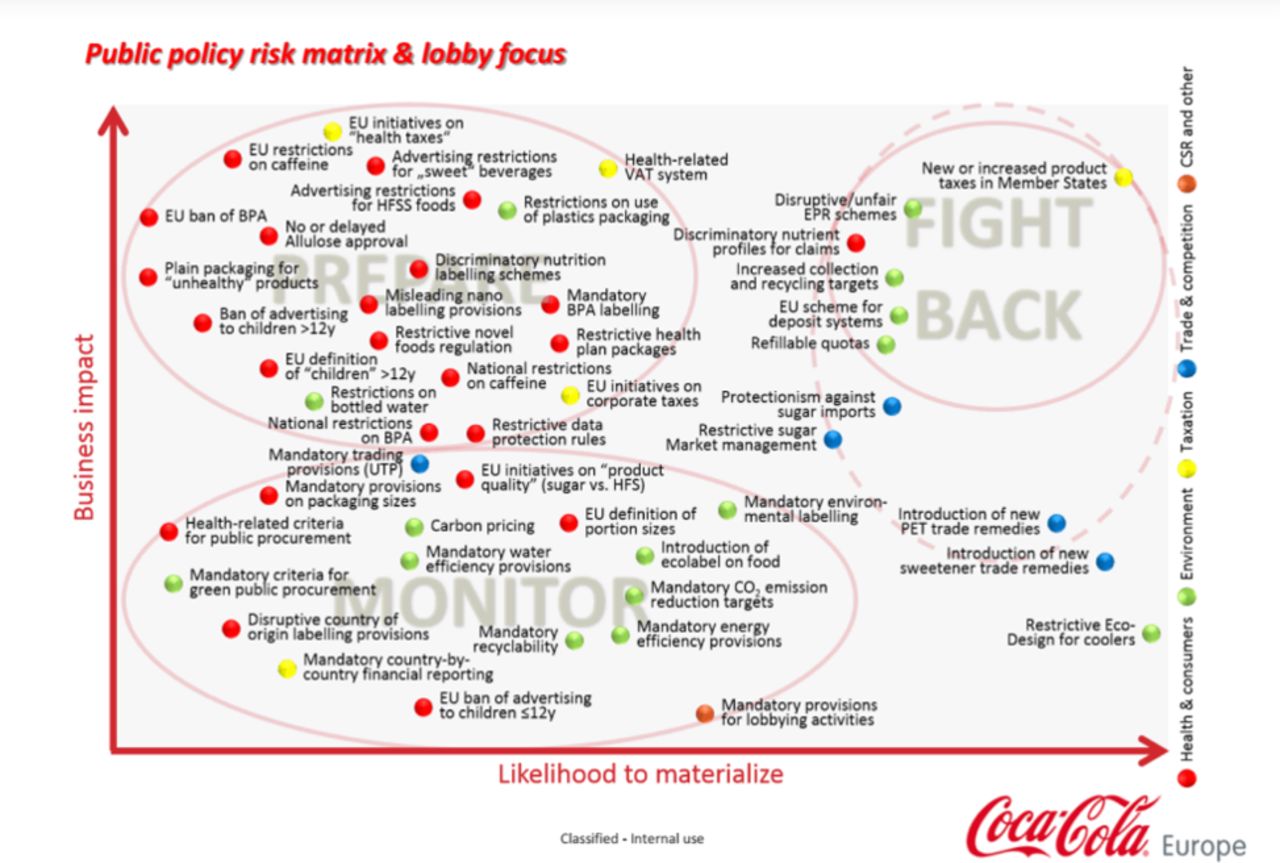

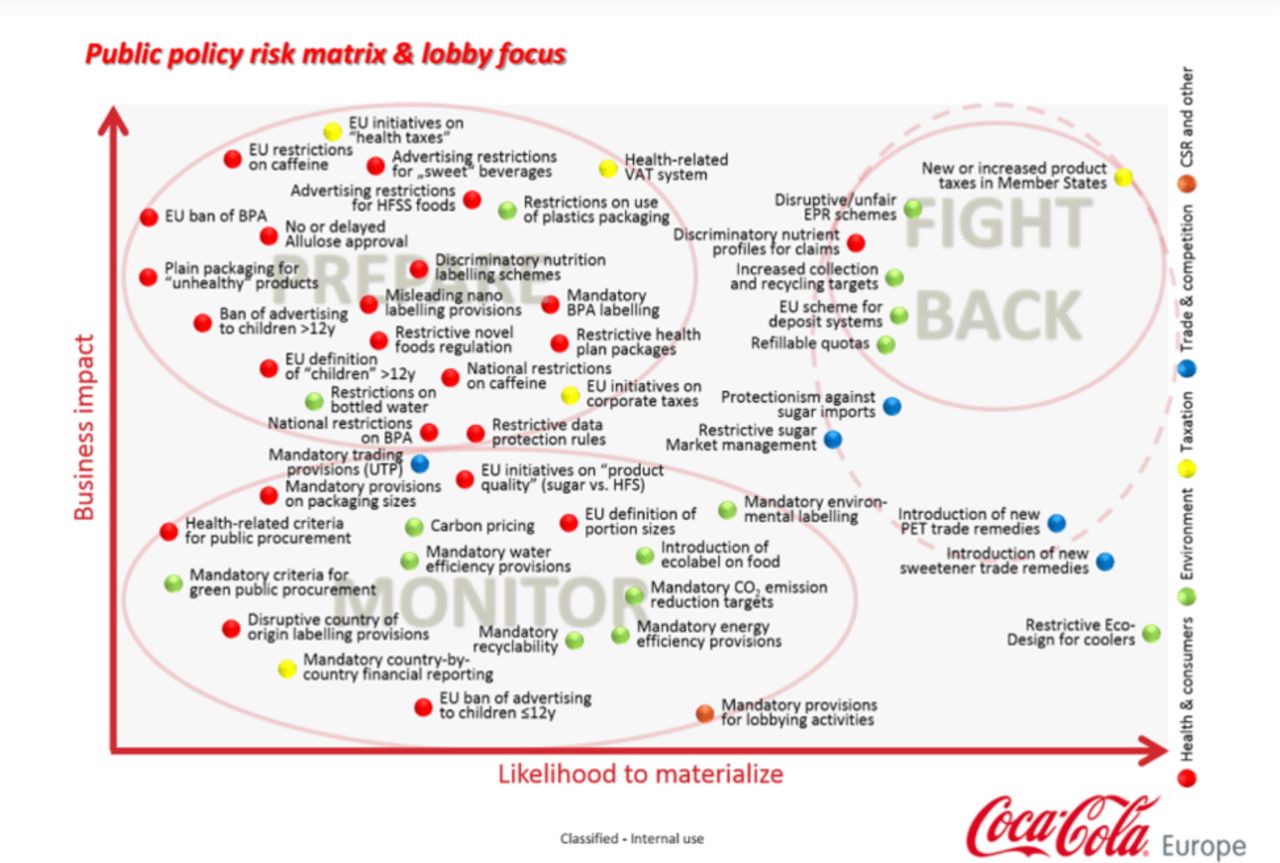

In January 2016, the WHO Commission on Ending Childhood Obesity issued recommendations that nation states consider soda taxes for the prevention of obesity and non-communicable diseases (NCDs).60 A February–March 2016 ‘classified—internal use only’ document underscored the degree to which Coca-Cola executives internally viewed soda taxes to be a significant threat to the company’s global enterprises. Figure 1 is reprinted from an international strategy document found in the Food Industry Documents Library, called the ‘radar screen’, which was produced by senior managers in Government Relations for Coca-Cola Europe. This radar screen was a ‘public policy risk matrix’. It compared 49 governmental policy threats to Coca-Cola’s business interests in the European Union (on the Y axis) against the likelihood that each could materialise in member countries (on the X axis). Notably, of all 49 public policy threats, new tax policies were assessed to have the greatest ‘business impact’ on Coca-Cola and were also assessed to have a strong ‘likelihood to materialise’.58

{kind=link}

Coca-Cola Europe: radar screen for monitoring public policy threats. Source: University of California San Francisco’s Food Industry Documents Archive.58 BPA, Bisphenol A; EU, European Union; HFS, high-fructose syrup; HFSS, high fat, sugar and salt; PET, Polyethylene Terephthala; UTP, Unilsted Trading Privileges; VAT, value added tax.

When a New York Times reporter expressed interest in ‘exploring the premise that there has been a rise in the number of city and state beverage tax proposals… (and) that this rise can be linked to the ‘success’ of the tax in Mexico’, the Vice President of Policy from the American Beverage Association (ABA) shared data from an industry-funded Mexican study34 showing that ‘the tax has failed to improve health as its proponents claimed, it is regressive and costs jobs’.61 Following an inquiry by the Wall Street Journal about the 2016 BMJ study showing the tax had decreased SSB sales, Coca-Cola’s Director of Global Affairs and Communications referred reporters to trade groups that had ‘multiple studies from well-respected institutions in Mexico (ITAM, COLMEX, UANL, supported by funding from industry) that make clear the tax was ineffective’.62 He also provided a pre-release study funded by the ABA showing that SSB consumption in Mexico had returned to its pretax baseline alongside 3000 job losses—claims that made their way into newsprint.62

When in 2017, the third peer-reviewed paper on the Mexican tax appeared in Health Affairs showing a sustained decline in SSB consumption over 2 years,13 the International Council of Beverages Association (ICBA) stepped in. As the main trade association for the global beverage industry, ICBA released a statement that ‘the study does not show any impact from the tax on the obesity rates in Mexico’, and called for alternative ‘evidence-based solutions’ via local partnerships between government and industry.63 Citing industry-funded studies, ICBA disseminated a fact sheet to its global partners outlining ‘a dozen reasons why soft drink taxes fall flat’.64

In 2018, in preparation for the United Nations (UN) high-level meeting on NCDs, global health commissions discussed soda taxation as an evidence-based NCD prevention strategy, citing peer-reviewed research on the Mexican tax.65 Internal email communications among Coca-Cola executives called this meeting ‘the most important event ahead in the NCD field’ and expressed concerns that the Mexican delegation was among ‘the most vocal proponents of restricting private sector engagement with the WHO’.66 In preparation for the high-level meeting, WHO released the report, Time to Deliver, which proposed ‘best buys’ for the prevention and management of NCDs, including tobacco and alcohol taxation.67 In a public comment, ICBA levied methodological criticisms of the Health Affairs paper on the Mexican tax, noting that ‘regrettably, the authors of this article are relying on a theoretical model’.68 WHO’s final report, Time to Deliver, stopped short of formally recommending soda taxes due to dissent by the US delegate,69 but noted ‘broad support from many Commissioners’.67

Contrasting messages from industry-funded and non-industry-funded research on the Mexican soda tax

Industry-funded reports, none of which were peer reviewed, became available within the first year of policy implementation. It was not until January 2016 that non-industry-funded evaluations of the Mexican tax policy began to appear in the peer-reviewed scientific literature. (See online supplemental table 2 for details on all studies.) We identified that the food and beverage industries funded studies that produced discursive strategies aligned to their interests, to play down the effectiveness of the Mexican soda tax (online supplemental table 3).

Industry-funded studies documented negative impacts of the soda tax on the Mexican economy, arguing that the policy will lead to lost jobs, store closures and affect the economy of the country, whereas non-industry-funded evaluations found none. For example, an industry-funded study, using an input–output econometric model, estimated that the tax had led to 10 815–42 385 job losses and an economy-wide loss of 6.4 billion pesos (US$378 million) during its first year, amounting to a 0.4% loss of Gross Domestic Product (GDP).33 In contrast, a non-industry-funded study analysed three nationally representative surveys to estimate changes in unemployment rates after adjusting for contextual variables. Authors found no significant employment changes associated with the tax, noting that sales of untaxed beverages had increased to ‘offset the potential negative effect on employment’.70

Industry-funded studies made arguments related to social justice, such as criticising the tax as regressive, and arguing that the policy was unfair to the poorest: even though tax revenues were collected ‘mainly from the richest households, the tax burden (was) heavier in the poorest households’.33 Industry-funded studies also argued that the ‘cost of the policy was particularly harmful in a situation that is notorious for the problems of inequity and poverty’.32 Conversely, the first non-industry-funded, peer-reviewed paper on the tax, published in 2016 by BMJ,12 found disproportionately large reductions in SSB purchases by lower-income households and concluded that this, plus health and productivity gains in these households, could potentially amount to a progressive, not regressive, tax effect.

Regarding public health benefits, two industry-funded studies33 34 and three non-industry-funded studies12 13 71 evaluated changes in SSB sales following implementation of the soda tax. Although all reported statistically significant reductions in SSB sales, which ranged from 3.4% to 7.3%, the interpretation of results differed depending on who funded the research. Industry-funded studies interpreted these declines as neglible, when calculated in terms of the calories they represented in an average Mexican’s diet, suggesting that it was meaningless from a health standpoint. Two industry-funded studies emphasised that no changes had been observed in rates of obesity during the first 2 years of the tax.33 34 Studies conducted by scientists without industry ties, in contrast, assumed that with such a small tax and only 2 years of implementation, empirical studies could not realistically be expected to find changes in obesity rates.72 However, three peer-reviewed non-industry-funded studies published modelling results that used observed declines in SSBs consumption to project the prevalence of obesity over a 10-year period, finding significant reductions.73–75

Conclusion

It is well documented that health-harming industries fund scientists to produce research to undermine new health regulations that, if enacted, could threaten commercial interests.22–24 76 77 The case of the Mexican soda tax shows that industry resistance can persist after new policies have become law as vested interests seek to roll back legislation, and to stall or prevent policy diffusion on an international basis. Immediately upon implementation, the same food and beverage industry stakeholders that had opposed passage of the Mexican tax took oversight positions on government advisory panels monitoring its effects and lobbied lawmakers to reduce the tax rate. Internal industry documents have shown that food and beverage executives feared the international diffusion of soda taxation and attempted to forestall its global diffusion by amplifying industry-funded research claims. They sought to combat emerging evidence that Mexico’s tax was effective. Ultimately, since Mexico implemented its tax, 35 countries have adopted similar measures.4 8

When health policy innovations are so new that they lack empirical research, industry-funded studies can be mobilised quickly to define an industry-friendly narrative.78–80 It took 2 years for independent evaluations of the Mexican tax to begin appearing in peer-reviewed scientific journals. In the breech, industry stakeholders within Mexico, supported by a global infrastructure of trade organisations and scientific front groups, were able to quickly generate credible-seeming evidence that the policy was a failure. Industry-sponsored studies, none of which were peer-reviewed, were rapidly published and disseminated at scientific meetings to establish a narrative that this policy was disproportionately affecting low-income households, producing job losses and lowering Mexico’s GDP, all while failing to lower SSB consumption or tackle obesity. This narrative drew on the image of neutral, unbiased science for legitimacy. Thus, when the Mexico-based scientific front group for the industry, ILSI Mexico, became too blatant in its efforts to undermine the tax, it was quickly censured and closed down.

Our literature review found that industry-funded studies routinely used discursive strategies to play down the effectiveness of the soda tax policy in Mexico. They issued economic (eg, loss of jobs), social justice (eg, tax is regressive) and public health arguments (eg, tax did not reduce obesity) similar to those previously used by the tobacco industry.26 27 81 Food and beverage industry interference went beyond simply ‘spinning’ emerging evidence of the tax’s effectiveness. Industry-funded research was cited within Mexico to encourage lawmakers to lower the tax—a proposal that passed in the Mexican Chamber of Deputies but failed in the Senate. Media outlets within Mexico were important for exposing industry’s recruitment of US-based scientists to advocate against the tax. This highlights the ongoing need to alert scientists, policy-makers and media outlets about conflicts of interest and why commercial interests can bias research.

Over time, industry-funded studies on Mexico were disseminated globally by beverage industry executives seeking to contain soda taxation within Mexico. As the threat of international diffusion grew, executives in transnational beverage corporations, such as Coca-Cola, aided by their global trade associations, amplified the narrative of a failed Mexican tax across their global communication networks. Industry-funded studies on Mexico were discussed in the international press during the run-up to the 2018 UN high-level meeting on NCDs, but by then, independent, peer-reviewed studies had provided competing evidence, resulting in a moderate degree of support for taxation.

Findings from this study underscore the decisive role that peer-reviewed research can play in implementing progressive public health policies. Mexico created a real-world context for the first peer-reviewed empirical studies demonstrating the effectiveness of taxing SSBs. Despite a notable degree of industry opposition, peer-reviewed evaluations of the Mexican tax eventually garnered the attention of international expert panels on NCDs.60 65 82 This gave impetus to measured endorsements of soda taxes by the UN and WHO, setting the stage for their growing adoption by countries around the globe.

Abstract translation

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.Data availability statement

Data are available in a public, open access repository.

Ethics statements

Acknowledgments

The authors are grateful to Kate Tasker and Rachel Takata of the University of California San Francisco's Industry Documents Library for archival support and assistance, and to Dr Cristin Kearns for substantive input on this research.

References

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Handling editor Seye Abimbola

Twitter @apedroz9, @MIALONMelissa, @acarriedo

Contributors All authors contributed to data collection, analysis, interpretation and revision for important intellectual content. LS, EC and AP-T drafted the manuscript.

Funding The work was supported by Bloomberg Philanthropies. AP-T has a scholarship from the Mexican National Council of Science and Technology (CONACyT377279). The funders had no role in design, conduct, collection, management, analysis and interpretation of the data or in the preparation, review or approval of the manuscript.

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.

Supplemental material This content has been supplied by the author(s). It has not been vetted by BMJ Publishing Group Limited (BMJ) and may not have been peer-reviewed. Any opinions or recommendations discussed are solely those of the author(s) and are not endorsed by BMJ. BMJ disclaims all liability and responsibility arising from any reliance placed on the content. Where the content includes any translated material, BMJ does not warrant the accuracy and reliability of the translations (including but not limited to local regulations, clinical guidelines, terminology, drug names and drug dosages), and is not responsible for any error and/or omissions arising from translation and adaptation or otherwise.