Article Text

Abstract

Introduction Several African countries have introduced universal health insurance (UHI) programmes. These programmes aim to extend health insurance to groups that are usually excluded, namely informal workers and the indigent. Countries use different approaches. The purpose of this article is to study their institutional characteristics and their contribution to the achievement of universal health coverage (UHC) goals.

Method This study is a narrative review. It focused on African countries with a UHI programme for at least 4 years. We identified 16 countries. We then compared how these UHI schemes mobilise, pool and use funds to purchase healthcare. Finally, we synthesised how all these aspects contribute to achieving the main objectives of UHC (access to care and financial protection).

Results Ninety-two studies were selected. They found that government-run health insurance was the dominant model in Africa and that it produced better results than community-based health insurance (CBHI). They also showed that private health insurance was marginal. In a context with a large informal sector and a substantial number of people with low contributory capacity, the review also confirmed the limitations of contribution-based financing and the need to strengthen tax-based financing. It also showed that high fragmentation and voluntary enrolment, which are considered irreconcilable with universal insurance, characterise most UHI systems in Africa.

Conclusion Public health insurance is more likely to contribute to the achievement of UHC goals than CBHI, as it ensures better management and promotes the pooling of resources on a larger scale.

- Health insurance

- Health policy

- Health systems

Data availability statement

No data are available.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

WHAT IS ALREADY KNOWN ON THIS TOPIC

Several African countries are implementing programmes to extend health insurance to the informal sector and the poor, but with difficulty given the specificity of the target population.

WHAT THIS STUDY ADDS

Our literature review identified African countries that have initiated universal health insurance (UHI) programmes.

We have summarised and analysed the way in which these African countries attempt to collect a maximum of resources and then pool them to guarantee access to care without financial difficulty for populations generally excluded from social security.

HOW THIS STUDY MIGHT AFFECT RESEARCH, PRACTICE AND/OR POLICY

The study identifies key challenges faced in implementing UHI schemes in African and other developing countries and points to the pitfalls to be avoided.

Introduction

Universal health coverage (UHC) is defined as the possibility for all individuals to have access to quality healthcare at an affordable cost.1 It requires equitable financing, that is, a sharing of costs within the population that considers the contributory capacities of everyone. All this implies the establishment of a prepayment system based on tax contributions or compulsory insurance contributions payable by employees, public or private employers and the self-employed.

In countries with a large informal sector, this social security type of health insurance is difficult to develop because, by definition, professional statuses and the individual tax base are difficult to identify.2 Another reason is to be found in the level of poverty of the populations. Indeed, economies characterised by a narrow formal sector generally have many poor people.3

Several strategies are being implemented to circumvent these challenges and achieve universal coverage through insurance. A series of studies, conducted between 2015 and 2017 by researchers mostly affiliated with the WHO, showed how, on different continents, countries were trying to expand health insurance beyond the formal sector. The studies covered Latin American countries,4 Asian countries,5 high-income countries in Eastern Europe6 and low-income and middle-income countries in Europe.7 For Africa, there are a few multicountry studies that describe and compare the institutional characteristics of insurance schemes for the informal sector.2 8–12 They show that there are four main models: community-based health insurance (CBHI), social security-type health insurance, public health insurance and private health insurance. However, behind these broad subdivisions, there are several specificities imposed by the socio-economic context, the political organisation or which are adaptations of foreign models.2

This paper follows on from the above studies and is intended to improve understanding of African models of insurance extension beyond the formal sector. However, the approach taken is broader than most studies published to date. Instead of discretionarily selecting a limited number of experiences to study, we start with all countries on the continent and look at how those countries that have implemented universal health insurance (UHI) programmes are proceeding. For the purposes of this paper, a programme qualifies as UHI if it is open to all segments of the population, especially to workers in the informal economy and the poor. Because of the diversity of approaches, but also because actors in different countries may name similar features differently or give the same name to different practices, we indiscriminately examine how schemes in each country that are open to people outside the formal sector collect, pool and use resources.2 4–7 We then compare the performance of the schemes in terms of the population covered the main objectives of universal coverage (access to care and financial protection for users) and the share of health expenditure covered by the health insurance schemes.

Our objective is to take stock of the different options for extending insurance in Africa, compare the approaches and try to identify those that are deemed to be the most successful.

Method

The present study is a narrative review of the literature.13 As a first step, a Google search was conducted to identify African countries where a UHI programme has been developed, that is, one that includes at least one scheme accessible to informal workers and the poor. The concepts of health insurance, health financing and UHC were associated with each of the 54 African countries to verify whether the country was eligible for the study. The research was conducted in French, English and Portuguese. Twenty-five countries were identified after this initial search.

Second, we excluded countries whose programmes were not insurance-based (Seychelles and Mauritius14 15), those whose programmes were still in the design phase (South Africa,16 Burkina Faso,17 Cameroon18 and Zambia19) and those whose programmes were recently established (Cote d'Ivoire,20 Egypt21 and Madagascar,22 that is, within 3 years. The remaining 16 countries included in the study are: Algeria, Benin, Burundi, Djibouti, Ethiopia, Gabon, Ghana, Kenya, Mali, Morocco, Nigeria, Rwanda, Senegal, Sudan, Tanzania and Tunisia.

The third step consisted of a literature search restricted to the 16 countries mentioned above. The search was conducted on PubMed, Google Scholar and EconLit. The following expression was used: (insurance) AND (universal coverage OR health financing OR impact OR evaluation) AND (Burundi OR Djibouti OR Ethiopia OR Gabon OR Ghana OR Kenya OR Mali OR Morocco OR Nigeria OR Rwanda OR Senegal OR Sudan OR Tanzania OR Tunisia). This search was done in English on PubMed and EconLit. On Google Scholar, it was done in English and French. Works published up to 2020 were retained. We excluded studies that focused on the determinants of insurance uptake and those relating to stakeholder perceptions. We retained only works that included an analysis of at least one of the institutional characteristics of UHI programmes or that evaluated their performance.

These studies were examined using the method of directed analysis,23 which consists of selecting in advance the themes about which information is to be collected. For the selection of these themes, we used the Health System Functions Framework developed by Kutzin.24 We were then interested in how the different schemes mobilise (collection function), pool (pooling function) and use financial resources (purchasing function) to achieve the main objectives of UHC.

Patient and public involvement

Patients or the public were not involved in the design, or conduct, or reporting, or dissemination plans of our research.

Research ethics approval

Our article is a narrative review of the literature. It does not involve human participants or animal subjects. Therefore, it did not require the approval of an ethics committee.

Results

Characteristics of the studies

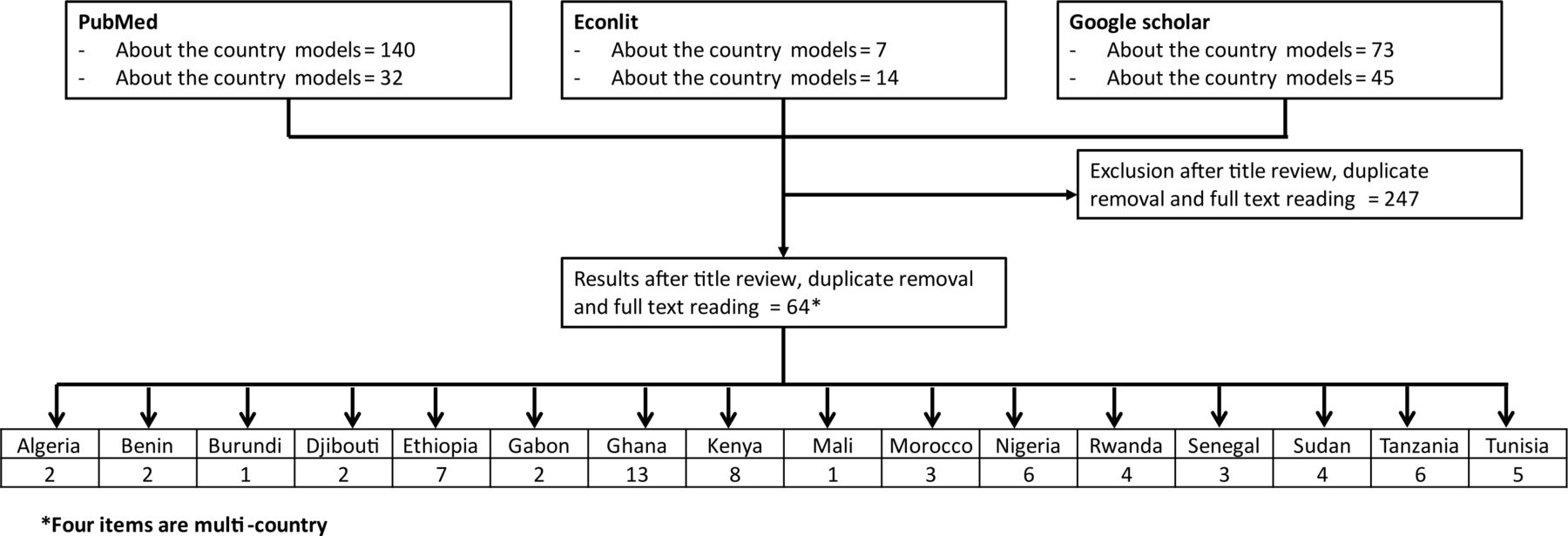

Three hundred and eleven publications were found through the various databases. After examining the titles, reading the abstracts or the full-text articles, 69 publications were selected. Four studies involved more than one country at a time. Figure 1 summarises the process of searching and selecting studies.

{kind=link}

Study selection process.

Resource collection function

The resources of the insurance schemes come from the insured, the State and foreign partners. As information on this external support is almost non-existent in the studies examined, only the results on the first two points are summarised here.

Contributions

There are three aspects that come up regularly: the compulsory or non-compulsory nature of the contribution, the way it is determined and its periodicity.

Nature of the contribution

A scheme is truly compulsory if those who are eligible for it ‘do not have the option of not being covered’25 because their enrolment is forced or automatic. Of the 16 UHI schemes studied, 9 are de jure compulsory (Algeria,26 Benin,27 Burundi,28 Djibouti,29 Gabon,30 Ghana,31 Kenya,32 Rwanda33 and Tunisia34). But, in fact, almost all these systems are voluntary. Indeed, of all the countries that have opted for compulsory membership, only Rwanda has provided for sanctions in the event of non-payment of contributions.35 36 In the other countries where insurance is compulsory, there are no provisions to force informal sector workers to contribute. In contrast, in Ethiopia, where insurance is officially voluntary, there are aspects of compulsory enrolment.37

Determination of the contribution

Unlike the health insurance schemes for formal sector workers, the contribution for the self-employed, especially those in the informal sector, is often a fixed lump sum, identical for all contributors, regardless of income level. This is the case in all the countries studied, except for Algeria and Rwanda. In the first country, the national social insurance fund for the non-salaried calculates the income of the insured based on the taxes due by the latter.38 But such a method is only suitable for the self-employed in the formal sector and cannot work for the self-employed in the informal sector, who pay almost no taxes.39 The Rwandan method is different. Flat-rate contributions have been set for three distinct income groups.35 36 Despite this, these flat-rate contributions are proving regressive36 and according to the results of a 2013 survey, 67% of contributors found the amount of premiums unbearable and 22% had even stated that they would not re-enrol.36

In other countries, the contribution for the informal sector is fixed and does not consider income levels, which often poses a problem of sustainability.40–43 In Senegal, contributions are not affordable for at least 40% of the population in some departments44 and 47% of respondents believe that the contribution is not sustainable.45 In Kenya, it has been shown that regardless of the financing approach, most informal sector workers will find it difficult to bear the contributions.32 46 In Ghana, on the other hand, 80% of National Health Insurance Scheme members interviewed for a study said that the contribution was reasonable.47

Periodicity of contributions

Annualisation of contributions is the principle for informal sector insurance schemes. This annualisation is a risk management measure that makes it possible to avoid a form of adverse selection whereby the beneficiary only contributes for periods when he is certain to need to use the insurance services.48 However, staggering the payment of the contribution makes the expense more bearable. For this reason, in Senegal,44 Nigeria,41 Ethiopia,49 Sudan40 and Rwanda,36 a contribution by instalments, which may even be monthly, is allowed.

Financing by public revenue

Depending on the country, public revenues are used to pay for indigent beneficiaries,35 36 42 50 51 to partially subsidise the contributions of non-indigent beneficiaries,49 50 52–54 to finance operating expenses43 52 55 or indiscriminately for all expenses.

States contribute to UHI mostly through their general revenues and we found earmarked taxes only in Gabon, Ghana and Rwanda.10 11 30 31 47 51 56 57 These are turnover taxes,10 31 47 58 royalties and the proceeds of some fines.

In some countries, local revenues are also a source of public financing for UHI schemes. In Senegal, several communes contribute to the financing of CBHI schemes, but at low levels and on a voluntary basis.59 In Ethiopia, local authorities subsidise the contributions of the indigent and the operating costs of CBHI schemes.37 49 52 In Tanzania, some districts pay the contributions of indigents, but the practice seems marginal.42 In general, local revenue financing of UHI programmes is not very developed in Africa.

Pooling function

Pooling models

Of the 16 countries surveyed, 11 have public insurance systems, 4 have CBHI systems and 1 has a private commercial health insurance system (table 1).

Classification of UHI models

Public health insurance models

Benefits in public health insurance systems are provided either by a national health insurance fund, a national social security fund or by branches of the central government. The countries that have opted for a national health insurance fund are Ghana,10 31 Kenya,32 Sudan,40 Morocco,60 Benin27 61 and Tunisia.34 62

In addition to this first group of countries, others have preferred to entrust the management of the universal insurance scheme to the national social security fund. These are Rwanda,35 36 Djibouti63 and Algeria.26 38 In Gabon, benefits are provided by a national health insurance fund which also manages the social protection services of persons receiving minimum social benefits.30 51

Burundi is the only country with a public insurance system that is not based on a fund. The scheme is managed directly by the central government, through its decentralised services.28

Private health insurance models

Nigeria is the only country included in the study that has outsourced the management of its insurance scheme to private operators.64 But the results fall short of expectations.65 In a survey of various categories of stakeholders who were asked to rate the quality of services provided by Health Maintenance Organisations on a scale of 1 to 5, 57.7% of respondents gave a score of 1.65

CBHI models

There are four countries with CBHI systems. These are Senegal,50 Ethiopia,37 52 Tanzania42 53 and Mali.66 67 In Senegal, a recent evaluation of the UHI programme conducted in conjunction with the government recommended moving to public health insurance, because of several weaknesses in the operation of mutual health insurance.68 Rwanda35 36 and Ghana,69 operated community-based insurance schemes for years before transitioning to public health insurance in 201535 and 2012,69 respectively.

The regulation and supervision of community welfare organisations is conducted on behalf of the State in most cases by an autonomous public agency. Only Rwanda had not opted for such a formula. The central services of the Ministry of Health played the role of regulator, supervisor and technical assistant to the health mutuals.36

Local authorities play a key role in managing, regulating or supervising the activity of the health mutuals in most CBHI systems. In Rwanda, until 2015,35 Ethiopia52 and Tanzania,42 the community-based insurance scheme is highly decentralised and structured around local governments. Unlike community-based schemes that are owned and operated autonomously by their members, community-based insurance in the above countries is a health insurance scheme based on a partnership between the central state and local governments on the one hand and the community on the other. The local authorities supervise the mutuals, monitor their activities, intervene in the recruitment of salaried staff and even determine certain technical parameters for the operation of the schemes in Ethiopia and Tanzania.54

Fragmentation

Fragmentation refers to the existence of different risk pools within the same population. There are various kinds of fragmentation in the countries studied. It exists between socio-professional groups, categories of the population, territories or between the health services covered.

There is a high degree of fragmentation in the community insurance systems. Since health mutuals are structured around local communities, there are at least as many pools as there are territorial subdivisions. In Senegal, there are 650 health mutuals, organised around 552 communes. There are therefore 650 different pools. In Ethiopia, there are as many pools as there are woredas.49 In Tanzania, each district constitutes a pool, that is, 169 separate pools.42 In,Rwanda, until 2015 there were 30 health mutuals for as many districts.36 In Ghana, under the CBHI system, there were 145 mutual health insurance schemes.70

Fragmentation is much less in public health insurance schemes. Pools are organised not by territory but by socioeconomic categories. In Gabon, the National Health Insurance Fund manages three pools, one for the formal sector, one for the informal sector and one for the indigent. The three schemes operate independently of each other; there is neither pooling of resources nor cross-subsidisation.51 In Kenya, the national health insurance fund also operates three schemes, one for civil servants, one for the indigent and a general scheme for the rest of the population, each offering different benefits.71

However, some countries have tried to reduce the fragmentation of their insurance systems by merging schemes or setting up cross-subsidy mechanisms. Among the countries that have attempted to defragmentation of schemes is Ghana in 2012, which moved to a single scheme for the whole country. Rwanda merged its 30 informal sector insurance schemes into a single scheme in 2015. In Sudan, health insurance was fragmented and there was a pool for each of the 18 states, with no real cross-subsidy. In 2016, all these pools were merged.63

Purchasing function

Benefits covered

In Senegal, the UHI scheme covers care provided in public health facilities, generic drugs sold by the pharmacies of these public facilities and drugs sold in private pharmacies.72 In theory, therefore, the package is broad. In practice, however, it includes several exclusions.72 Expensive hospital care is not covered by mutual organisations, and drugs prescribed for the treatment of chronic diseases and expensive medicines are generally not reimbursed. Coverage is thus limited to services offered by primary healthcare facilities, hospital consultation and some non-expensive hospital services. Beneficiaries are covered only for care received in health facilities approved by their mutualist organisation of affiliation. There is no portability of insurance.72 This implies that the insured can only be treated in his place of residence and that in case of temporary travel, his insurance does not cover him.

In many other countries, coverage is limited to primary care and is limited to the locality of enrolment. Geographical portability is absent when fragmentation is geographic. Funds only cover services offered in the locality of enrolment.44 52 53 73

The packages covered are not always identical from one group to another. This is the case in Sudan,40 Tanzania53 and Tunisia63 where the schemes offer different services.

Methods of remuneration for providers

Fee-for-service payment is the main method of payment in the systems studied. It is dominant in Senegal,72 Gabon,51 Nigeria,41 Rwanda,36 Tanzania42 and Tunisia.63 The second most common method of remuneration is a lump-sum subsidy that is not correlated with the services provided. Healthcare providers receive a global envelope in exchange for the care they provide to the insured of the scheme. This is the case in Morocco60 and Algeria.38 In Tanzania, a similar approach is applied.42 Healthcare providers are not reimbursed for services provided to CBHI beneficiaries, but they are entitled to use the resources pooled at the district level under the CBHI scheme.

Co-payment

In Ethiopia and Ghana, there is no copayment for access to care,31 49 although in both countries, studies report that the stakeholders advocate its introduction.31 49 Burundi has reintroduced the copayment whereas at the beginning of the programme it did not exist.28 In Sudan, there is no copayment except for medicines.40 55

In all the other countries, copayments exist but according to different modalities. It can be a flat rate28 38 54 or a rate that varies according to the service requested44 or the level of the health pyramid.27 30

Several countries have exemptions from copayment. They are granted to the indigent in Algeria,38 Rwanda36 and Gabon (on request).30 They apply to specific services: expensive procedures in Algeria38 and Tunisia,74 primary healthcare in Benin27 and maternity care in Gabon.30

Progress towards universal health coverage

Population covered

Coverage rates (or to be more accurate enrolment rates) by all insurance schemes in the countries studied are from 3% to almost 90%. Nigeria and Mali have the lowest rates, with 3%11 64 and 7% of people covered respectively.66 Rwanda, Algeria and Tunisia have the highest rates with results above 80%. Table 2 presents the results by country, all population categories included.

Universal health insurance enrolment rate and poverty rate

The studies do not usually provide coverage rates by subgroup. They may indicate the distribution of eligible populations by category, but give little indication of detailed coverage rates, except for the poor, who often benefit from a free care scheme. In Senegal, for example, nearly 19% of the population is enrolled in the indigent scheme of the UHI programme.50 In reality, however, coverage is not effective for most of these beneficiaries, in particular because the community mutual health insurance companies put up barriers to access due to delays in the payment of subsidies by the government.75 Tunisia, Gabon and, to a lesser extent, Rwanda, are the best performers in the cohort. In Gabon, more than 90% of those eligible for the indigent scheme are covered, which corresponds to about 27% of the population.30 Tunisia, with 22% of the indigent enrolled, is another system that has managed to enrol almost all the poor.74 Rwanda has managed to enrol an almost similar proportion (24%) of its population as indigent,36 but the levels of poverty are different, so the performance of the two countries is not comparable. In Morocco, 19% of the general population is covered by the destitute scheme, less than the 30% of the population that had declared itself eligible for the scheme.60 For the other countries, on the other hand, less than 10% of the population is registered as poor in the UHI programme27 28 47 49 52 55 while the number of poor people (table 2) is higher.

Care use and financial protection

We were able to review studies that analysed the performance of UHI programmes in 9 out of 16 countries. These were Ethiopia, Ghana, Kenya, Morocco, Nigeria, Rwanda, Sudan, Tanzania and Tunisia. For all these countries, insurance schemes were found to increase the likelihood of using health services and to improve the financial protection of the insured.

In Ethiopia, studies have shown that CBHI beneficiaries are more likely to use health services than the uninsured,76 77 especially outpatient services.78 They also have lower out-of-pocket payments76 79 and are less exposed to catastrophic health expenditures.79 In Ghana, health insurance has a positive effect on the use of care,80 particularly hospitalisation,81 antenatal care,80 82 skilled birth attendance82 and drugs.81 It increases the probability of access to both public and private facilities for the insured,83 improves access to care for children84 and the poor85 and reduces self-treatment.83 On the objective of financial protection, most studies have also concluded that there is a positive effect of the health insurance programme,80 81 86 even for the poorest.87 There are, however, a few studies that have reported a lack of significant effect of insurance on out-of-pocket payments,88 particularly on out-of-pocket spending on drugs.86 In Kenya, studies have shown that insured people are more likely to use health services than uninsured people,89 except for hospitalisation services.89 The Kenyan health insurance programme also promotes access to maternal healthcare in private hospitals90 and reduces out-of-pocket health expenditures.91 In Morocco, the only impact study we included in this review found a significant impact of insurance on catastrophic health expenditure.92 In Nigeria, the public health insurance scheme is also reported to have an impact on access to care and financial protection for beneficiaries,93 except for the poor.93 Such a lack of equity was also observed in Rwanda, where policyholders in the poorest quintiles used less care than other policyholders and were more exposed than the latter to catastrophic health expenditure.94 However, apart from this equity issue, several studies have concluded that in Rwanda the health insurance programme had a positive effect on access to care,94 particularly for children,95 and on financial protection,94 especially protection against catastrophic expenses.94 In Sudan, health insurance was found to have an impact on access to care,96 even in the case of chronic diseases.96 Access to care provided by private providers is made easier by the insurance programme except for outpatient care.96 In Tanzania, a study showed that health insurance had an impact on access to care and financial protection.97 Finally, the same finding was made in Tunisia where, in addition, health insurance would increase the probability of accessing private care and protect against catastrophic expenses related to chronic diseases.34

Share of health expenditure covered by health insurance schemes

We also collected information on the share of current health expenditure borne by health insurance schemes (table 3). Among the countries studied, Gabon, Tunisia and Morocco have the highest contribution of health insurance schemes to current health expenditure (35.9%, 33.8% and 30.1%, respectively). Ethiopia, Burundi and Nigeria, on the other hand, have the lowest share of health expenditure borne by health insurance schemes (1%, 1.9% and 2.9%, respectively).

Share of health insurance schemes expenditures and out-of-pocket payments on current health expenditures in 2019 (Source: WHO, Global health expenditure database)

Table 3 also shows the share of out-of-pocket payments in health spending for the 16 countries studied. Rwanda has the best performance in this area (11.67%) which places it at the same level as the best models in the world on this indicator. Nigeria and Sudan, on the other hand, have the highest rates in the group (70.52% and 67.38%).

Discussion

The objective of this study was to identify the main characteristics of UHI schemes in Africa. By systematically examining how these schemes raise, pool and use resources, we aimed to identify major trends, promising options and those that are less successful.

One of the main findings is that in all the countries studied, the resources mobilised by insurance schemes remain small and contribute only a small share to current health expenditure. In fact, in almost all African countries it is illusory to rely on contributions to achieve universal insurance, particularly given the size of the informal sector and the low contributory capacity of a large part of the population.8 98

In order to mobilise the maximum possible contributions, most of the countries included in the study are trying to implement the frequent recommendation to make insurance enrolment compulsory.1 33 98–101 But such a decision, as the results of our study have shown, is purely theoretical. It is not enough to say that a plan is mandatory for it to be so.102 If it is a contributory scheme, it is necessary that the targeted individuals cannot avoid their obligation to contribute and that, in addition, there is a mechanism for free coverage of the indigent.102 A compulsory collection scheme generally has two mechanisms: one in which the insured’s contribution is deducted at source, that is, automatically from his income by his employer or his principal (for self-employed providers), without him having the possibility of objecting; and a second in which the insured is obliged to pay his contribution, on pain of a penalty, generally in the form of a fine added to the contribution debt, both of which can be recovered by compulsory enforcement if necessary.103 The first mechanism is impossible to implement on a large scale with a very large informal sector, which is the case in the various countries studied.102 It is therefore necessary to find a way to force potential members to contribute, even if they have no formal income. Our study has shown that only Rwanda has succeeded in doing so for the moment, and even there it seems difficult for a large proportion of the insured to pay the contribution.35 36

Finally, the solution to mobilise more resources is to opt for a system financed by taxes, at least for a large part.98 A consumption tax could replace contributions and ensure an indirect contribution from the informal sector.35 And, to reduce the regressive nature of these taxes, exemptions or reduced rates for basic necessities could be considered.104

Our study also showed that in African countries with UHI programmes, the dominant model for managing risk pools is public health insurance. CBHI systems do exist, but they are community-based in name only. The prominent role of communities, which is the main feature of CBHI, tends to be reduced. Rwanda experimented with the pure form of a community-based mutual in the early 2000s, and then quite quickly moved to mutual health insurance schemes that were in fact only community-based in name.35 36 The management of insurance operations by civil servants, the preponderant role of the municipalities and, in general, the confinement of users’ representatives to social mobilisation and supervision activities was done in the first 5 years of UHI’s existence.36 The success of the Rwandan model is therefore wrongly presented as proof of the effectiveness of community insurance.33 35 Significantly, Rwanda transferred the management of health insurance for the informal sector to a public fund in 2015, as Ghana had done 3 years earlier. Senegal and Mali are currently the only countries with a UHI programme that relies on the pure form of CBHI.66 Ethiopia and Tanzania have CBHI systems under the supervision of local authorities and managed by employees recruited or paid by the latter.42 52 In fact, CBHI no longer seems to be considered an effective system for achieving universal coverage.33 105 Confidence in the ability of health mutuals to be the funds for UHI has eroded. However, as our results show, the creation of a public fund is no guarantee of success, and the absence of a public fund is not a source of failure. The success of a UHI plan depends on multiple factors. When it comes to pooling resources, one of the critical aspects is the level of fragmentation of the schemes.

High levels of fragmentation undermine risk sharing and cross-subsidisation between different income groups.32 It also promotes non-portability of care, that is, insurance organisations only cover services available in the locality of enrolment.44 52 53 73 Fragmentation can also create inequity, as the packages covered are not always the same, as we have seen from one locality to another in Senegal72 or from one group to another in Sudan,40 Tanzania53 and Tunisia.63 Minimising fragmentation is therefore essential to achieving universal coverage. However, this is less easy to do with a CBHI system.25

This is one reason why a growing number of studies question the effectiveness of CBHI, at least in its pure form.33 35 105 106 At a minimum, our results confirm that CBHI performs worse than public health insurance. Indeed, our results show that in countries with public health insurance, insurance schemes contribute more to health expenditures than in countries with CBHI (19.75% vs 6.56%). Our results also show that if we compare the share of out-of-pocket payments in healthcare expenditure, public health insurance systems perform better than CBHI systems (34.24% vs 35.59%). This is also the case when comparing the average enrolment rates of the insurance schemes (23.21% for CBHI schemes and 48.8% for public health insurance schemes).

However, a major limitation on the comparison of enrolment rates must be noted. The ways in which rates are determined vary from one country to another. The level of services covered at which beneficiaries are considered insured are not the same. In Senegal, the free care scheme for children under 5 years of age focuses on primary care and is included in the calculation of the national enrolment rate.75 In Kenya, where there is free access to primary healthcare, if the Senegalese calculation method had been applied, it would have been possible to consider that 100% of the population was covered. However, a coverage rate of 19% is used.32 Under what conditions can a person be considered insured? Countries have different approaches, which means that comparing coverage rates is not informative, and it is not clear that a country with a higher rate than another is better than the latter.

In addition to these limitations on the comparison of coverage rates, we can mention some others. This is the case for the type of review chosen for this study. We opted for a narrative review, instead of a systematic review, given the broad scope of the subject. This necessarily results in some limitations, namely the non-exhaustiveness of the research and the possible subjectivity in the choice of the studies examined. Another major limitation of the study is that many of the countries compared have various levels of income and current health expenditures. Comparing their performance should therefore be done with caution.

Conclusion

Our review of the literature found that public health insurance is more likely to contribute to the achievement of UHC objectives than CBHI because, among other things, it reduces duplication of management costs, promotes portability of care, enhances management transparency, and reduces fragmentation. However, to validate these findings, more research is needed, such as a comparison of the impacts of coverage schemes in Ghana and Rwanda before and after the transition from community-based to public health insurance.

Data availability statement

No data are available.

Ethics statements

Patient consent for publication

Ethics approval

Not applicable.

References

Footnotes

Handling editor Seye Abimbola

Contributors All authors contributed to all stages of the writing of the article. MSL is the guarantor of the overall content and controlled the decision to publish.

Funding The authors have not declared a specific grant for this research from any funding agency in the public, commercial or not-for-profit sectors.

Competing interests MSL is an employee of the Senegalese public agency for universal health insurance.

Patient and public involvement Patients and/or the public were not involved in the design, or conduct, or reporting, or dissemination plans of this research.

Provenance and peer review Not commissioned; externally peer reviewed.