Article Text

Abstract

Background While the COVID-19 pandemic may have substantially hindered the provision of routine immunisation services worldwide, we have little data on the impact of the pandemic on vaccine supply chains.

Methods We used time-series analysis to examine global trends in vaccine sales for a total of 34 vaccines and combination vaccines using data from the IQVIA MIDAS Database between August 2014 and August 2020 across 84 countries. We grouped countries into three income-level categories, and we modelled the changes in vaccine sales from April to August 2020 versus April to August 2019 using autoregressive integrated moving average models.

Results In March 2020, global sales of vaccines dropped from 1211.1 per 100 000 to 806.2 per 100 000 population in April 2020, an overall decrease of 33.4%; however, the vaccine sales interruptions recovered disproportionately across economies. Between April 2020 and August 2020, we found a significant decrease of 20.6% (p<0.001) in vaccine sales across high-income countries (HICs), in contrast with a significant increase of 10.7% (p<0.001) across lower middle-income countries (LMICs), relative to the same period in 2019. From August 2014 through August 2020, monthly per capita vaccine sales across HICs remained, on average, at least four times higher than in LMICs and nearly three times higher than in upper middle-income countries.

Conclusion Our study revealed the heterogeneous impact of COVID-19 on vaccine sales across economies while underlining the substantial consistent disparities in per capita vaccine sales before and during the first wave of the COVID-19 pandemic. Action to ensure equitable distribution of vaccines is needed.

- vaccines

- COVID-19

- health systems

- public health

Data availability statement

Data may be obtained from a third party and are not publicly available. Data can be obtained through IQVIA.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Key questions

What is already known?

Vaccine distribution is at risk of disruption during a global health emergency.

Supply constraints are an essential aspect of the health system that could limit service uptake.

What are the new findings?

Shortly after the COVID-19 pandemic declaration, vaccine sales plummeted globally by over 33% in April 2020.

The overall impact of COVID-19 on vaccine supply chains was heterogeneous across economies.

Between April 2020 and August 2020, high-income countries (HICs) experienced a significant decrease of 20.6% in overall vaccine sales, in contrast with a 10.7% significant increase across lower middle-income countries (LMICs), relative to the same period in 2019.

Between August 2014 and August 2020, the monthly per capita vaccine sales in HICs were, on average, at least four times higher than in LMICs and nearly three times higher than in upper middle-income countries.

What do the new findings imply?

If vaccine sales continue to mirror the current per capita figures, more disparities across economies would be prevalent.

Action to ensure equitable distribution of vaccines is needed.

Introduction

Vaccination is one of the most important public health interventions that has significantly reduced the burden of infectious diseases worldwide.1 2 The universal administration of these vaccinations remains a cornerstone of public health globally. More recently, the COVID-19 pandemic has significantly impacted the global economy and disrupted health systems worldwide. Most countries are yet to recover from the immediate effects of SARS-CoV-2 that has infected at least 220 million people worldwide and caused over 4.5 million deaths by the end of August 2021.3 Countries were affected by the pandemic differently, as evidenced by the disproportionate effects of the virus on populations,4 and the success—or lack thereof—to contain the spillovers of the pandemic has been linked with governance systems.5

During a period of intense pressure on health systems, significant resources were repurposed to combat the increasing influx of patients with COVID-19, limiting attention to other health priorities. While vaccination coverage has stagnated over the last decade and remains far from complete in many countries,6 the surge of the COVID-19 pandemic has temporarily and justifiably disrupted vaccine delivery.7 Not only were routine immunisation activities affected but also preventive vaccination campaigns were suspended.8 9 Primary healthcare enforced triage and the administration of routine vaccines dropped significantly during the early stages of the COVID-19 pandemic,10 11 together with declines in childhood visits and vaccination coverage.12 13 Several organisations have highlighted the increased vulnerability of children to vaccine-preventable diseases threatened by the emergence of COVID-19.7 14 The impact of the pandemic and associated disruptions on child vaccination were unprecedented, leaving 22.7 million children missing out on vaccination, 3.7 million higher than in 2019 and the highest recorded number of unvaccinated and undervaccinated infants since 2009.8

Reported reasons for COVID-19-induced disruptions to immunisation include an interplay of multiple factors such as reasonable concerns of COVID-19 infection and transmission, lockdowns and mobility restrictions, and limitations to service provision and immunisation outreach activities.12 15 Further, COVID-19 has imposed a strain on global manufacturer production capacities, supply availability and distribution. As a result of flight cancellations, border closures and transport disruptions, countries’ and suppliers’ shipment plans were significantly impacted.16 Demand for drugs was severely affected, and pharmaceutical shortages shed light on the flaws in the global supply chain that could compromise the response to new waves of COVID-19 and other pandemics.17 In the context of a public health emergency, governments and international organisations are faced with a series of challenges, including supply chain and logistics associated with safe storage, deployment, administration and disposal of vaccines.18

The impact of the COVID-19 pandemic on the fragility of the global vaccine supply chain in responding to a pandemic is yet to be unravelled with real-world data. This study focuses on vaccine sales as a key pillar to vaccine supply during a period of paradigm shifts in demand and uncertainties in their production and deployment. Our analysis aims to provide a regional view of the impact of the COVID-19 pandemic on vaccine sales across 84 countries and the ongoing dynamics of vaccine sales before and during the pandemic.

Methods

Data sources and setting

We used data from the IQVIA MIDAS Database between August 2014 and August 2020. This dataset included monthly vaccine sales from 66 countries and 2 geographical regions (Central America (N=6 countries) and French West Africa (N=12 countries)). On average, IQVIA MIDAS Database covers 89.5% of all country-level retail and hospital-based pharmaceutical sales across its market coverage. It is reconciled for returns and is validated against alternate sources.19 20 More information describing the IQVIA MIDAS sales data can be found in the online supplemental appendix A.

Supplemental material

We used the 2021 World Bank (WB) country classification of economies to group countries into distinct income-level categories as characterised by their gross national income per capita.21 The countries for which data were available fell into three economies: high-income countries (HICs), upper middle-income countries (UMICs) and lower middle-income countries (LMICs). We did not group the two geographical regions under the WB classification as they include a congregation of countries that fall into different income-level categories (online supplemental table 1). Nevertheless, we accounted for these regions under the ‘All regions and countries’ category. We excluded Venezuela as it experienced high hyperinflation rates during our study period (data not shown).

We defined monthly vaccine purchases using standardised units (ie, single doses or vials) of retail vaccine sales, and we estimated midyear population sizes based on the United Nations 2019 Urbanization Prospects.22 We included a total of 34 infants, adolescents, adults and all age group vaccines, as recommended by the WHO. The WHO routine vaccine schedule lists the recommended vaccines for all immunisation programmes, certain geographical regions, high-risk populations and immunisation programmes with certain characteristics.23 Given the wide-ranging indication of seasonal influenza vaccine, recommended yearly for individuals aged 6 months and above,24 it accounted for the major market share of vaccine sales across HICs. Additionally, given the large variation in influenza burden and seasonality differences by country, we excluded seasonal influenza vaccine since it could make the comparison more challenging. Nonetheless, we presented the results including seasonal influenza vaccine in the online supplemental figure 1 and appendix B.

Statistical methods

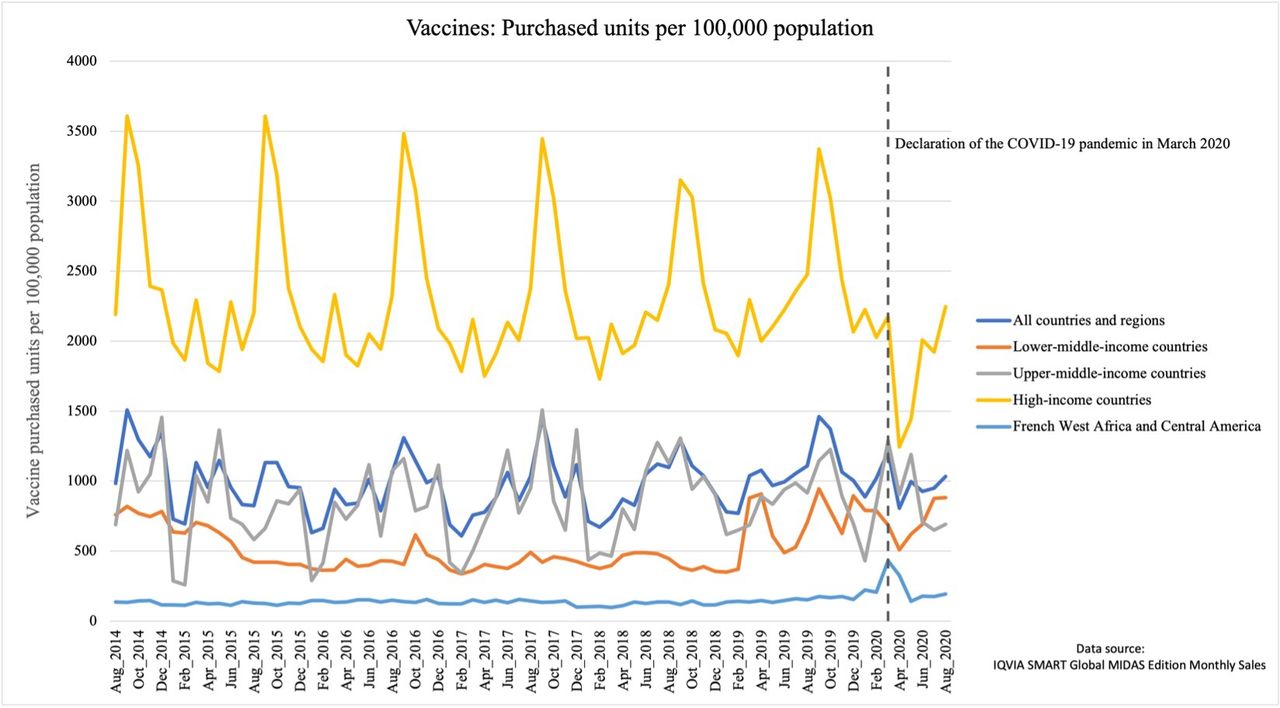

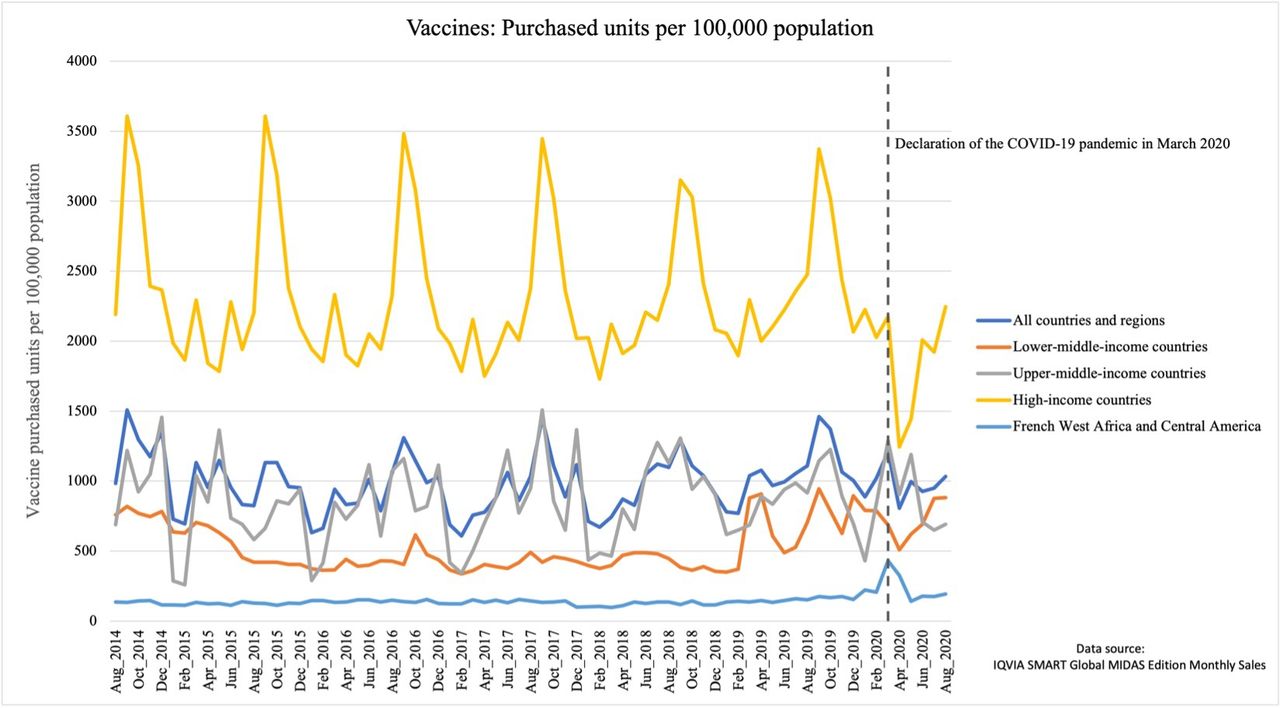

We used time-series analysis to investigate the impact of the COVID-19 pandemic on global vaccine sales.25 We plotted monthly purchased standard units of vaccines per 100 000 population by the WB classification of country-income levels and geographical location (figure 1 and online supplemental figure 1) from August 2014 to August 2020. For each vaccine, we constructed measures of relative changes in per capita vaccine sales defined as the difference in the number of vaccine units per 100 000 population purchased in a time period of 2020 relative to the same period in 2019. Further, we mapped the percentage changes in vaccine sales trends in the early stages of the COVID-19 pandemic. Additionally, we reported month-to-month comparisons in overall rates of vaccine sales by country from February through April 2020 relative to 2019.

Average per capita vaccine sales between August 2014 and August 2020 by country income level category.

Following visual presentation, we used autoregressive integrated moving average models to evaluate relative temporal trends in vaccine sales. Based on our model, we estimated percentage changes in vaccine purchases across all surveyed countries falling into each of the three income-level categories between April and August 2020, relative to the same period in 2019. For each vaccine, sales trends were plotted against time by income-level categories to detect the non-stationarity of time series. To determine the trends in vaccine sales, we fit a ramp function (April through August 2020 vs 2019) in the models. We fitted four models of different orders and selected the model with the lowest Akaike information criteria.26 All models were implemented using SAS V.9.4.

Patient and public involvement

Prior to initiating this research, we engaged multiple stakeholders from healthcare organisations, academic institutions and non-governmental organisations. These stakeholders were involved in identifying the research questions in our analyses.

Results

Global vaccine purchases

Time series plotted in figure 1 shows vaccine sales between August 2014 and August 2020 across countries covered by the MIDAS Database. Globally, the total number of vaccines purchased monthly ranged between 37.7 million and 91.8 million units, with an average (SD) population-standardised vaccine units of 989.2 (200.3) per 100 000 population. Following the declaration of the COVID-19 pandemic by the WHO in March 2020, global sales of vaccines dropped from 1211.1 per 100 000 population to 806.2 per 100 000 population in April 2020, an overall decrease of 33.4% (figure 1). Between April and August 2020, global trends in vaccine sales showed an overall significant decrease of 9.5% (p<0.001, table 1) relative to the same period in 2019. Vaccine purchases for all vaccines decreased globally except for the combined diphtheria, tetanus, pertussis (DTP)–hepatitis B that experienced a significant increase of 23.5%. The WHO recommended vaccines for all immunisation programmes, including BCG, DTP, diphtheria and the combined diphtheria–tetanus–polio experienced global decreases in sales. The WHO recommended vaccines for certain geographical regions, including yellow fever, Japanese encephalitis and tickborne encephalitis, also experienced significant global reductions in sales. The pattern is similar for vaccines recommended for some high-risk populations such as typhoid, varicella and hepatitis A. These global sales reductions ranged from 9.1% to 82.5% (table 1 and online supplemental figure 3).

Changes in per capita vaccine sales between April and August 2020 when compared with the same period in 2019, by countryincome level category

Income-level heterogeneity of vaccine purchases

Between August 2014 and March 2020, the rate of vaccine sales across HICs averaged (SD) 2314.9 (488.1) units per 100 000 population as compared with 852.1 (293.9) per 100 000 population in UMICs, and 524.4 (168.0) per 100 000 in LMICs (figure 1). The wide discrepancies in vaccine sales pattern held in the post-pandemic period. Between April 2020 and August 2020, the average monthly per capita vaccine sales in HICs was 1772.1 (371.7) per 100 000 population, equivalent to over double the vaccine sales rates across both UMICs with 828.6 (200.9) per 100 000 population and LMICs with 716.6 (145.6) per 100 000 population.

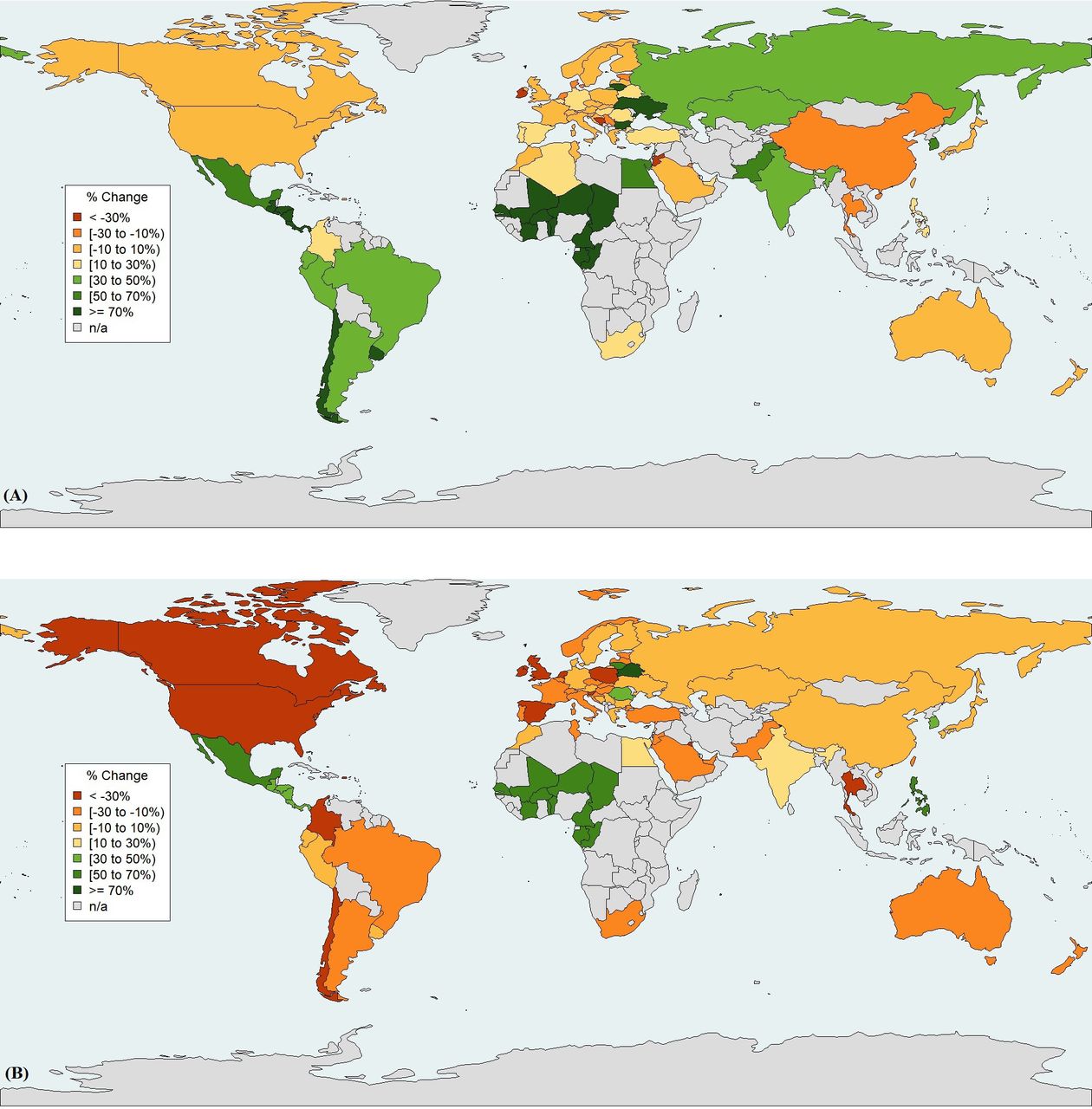

The percentage changes in per capita vaccine sales from January to March 2020 and from April to August 2020 relative to the same periods in 2019 are mapped in figure 2A and figure 2B, respectively. There is a striking contrast between economies, with most HICs experiencing a relative decrease in vaccine sales in the early stages of the pandemic. Notably, the USA, Canada, New Zealand, Australia, and select countries in Europe such as Ireland, Poland, UK, the Netherlands, Slovenia, Spain, Norway, Czech Republic, Belgium, and Hungary had over 25% relative decrease in overall vaccine sales. Meanwhile, Belarus, the Philippines, Lithuania, Mexico, Korea, Romania, French West Africa and Central America had over 30% increase in vaccine sales in the same period relative to 2019 (figure 2B and online supplemental figure 4).

{kind=link}

{kind=link}

Global trends in model-based estimates of the percentage change of per capita vaccine purchases (excluding seasonal influenza vaccine) between the post-pandemic and pre-pandemic period. No data were available for the countries in grey. Data source: IQVIA SMART Global MIDAS Edition Monthly Sales. (A) Global changes of per capita vaccine sales in January–March 2020 as compared with January–March 2019. (B) Global changes of per capita vaccine sales in April–August 2020 as compared with April–August 2019.

As shown in table 1, the pattern in vaccine sales in the first months of the pandemic differed across economies. UMICs experienced a non-statistically significant overall decrease of 9.3% in vaccine sales, with the estimated changes across vaccine type shuffling with no apparent trend. Interestingly, the model-based estimates of the percentage change in the rate of vaccine sales revealed a significant increase of 10.7% (p<0.001) in vaccine sales across LMICs, in contrast with a significant decrease of 20.6% (p<0.001) across HICs, in April–August 2020 relative to the same period in 2019 (table 1).

Various patterns in vaccine purchases by recommendation

Vaccines recommended for routine immunisation for children experienced significant decreases in sales across both HICs and LMICs. The hepatitis B vaccine, recommended for all children worldwide, with the first dose administered immediately at birth followed by two or three doses to complete the vaccination series, experienced significant sales decreases of 21.6% and 31.1% across LMICs and HICs, respectively. The hepatitis A vaccine, routinely recommended for children in highly endemic hepatitis A countries or travel-related purposes to these areas, experienced significant sales decreases of 24.7% and 50.7% across LMICs and HICs, respectively. Meningococcal vaccine, recommended for children in some immunisation programmes or required for travel-related purposes to certain areas, experienced significant sales decreases of 39.4% in LMICs and 19.4% in HICs. Measles, mumps and rubella (MMR) vaccine sales significantly dropped by 21.4% and 29% across LMICs and HICs, respectively, and the monovalent rubella vaccine sales decreased by 29.2% in LMICs. Nevertheless, the crude volume of MMR vaccines was notably higher in HICs with 498 units per 100 000 population, as compared with 18.2 units per 100 000 population in LMICs in the first months of the pandemic. Except for tetanus, rabies and the combined DTP–Haemophilus influenzae type b (Hib), the wide disparities in the per capita vaccine sales between HICs and LMICs were observed with every vaccine included in this study.

We also detected divergent and distinct patterns in the sales of routine vaccines and vaccine-preventable diseases across economies. A minor increase in relative vaccine sales for pneumococcal (3.9%) and rotavirus (1%) vaccines was observed in HICs as opposed to a decrease of 15.8% and 21.5%, respectively, in LMICs. BCG vaccine sales administered immediately after birth in most LMICs increased by 13.9% in LMICs. In contrast, the human papillomavirus (HPV) vaccine, recommended for girls aged between 9 and 14 years old and boys in some countries, experienced a significant drop of 44.6% in sales in LMICs. The monovalent tetanus vaccine, recommended for wound management for adults, experienced a significant sales drop of 22.6% in HICs.

Our analysis also showed a considerable reduction in the sales of travel-related vaccines across HICs. In the first few months of the pandemic, the sales of travel-required yellow fever vaccines fell by 84.7%. Moreover, the sales of travel-recommended vaccines such as typhoid and rabies decreased significantly by 93.9% and 67.7% in HICs, respectively (table 1).

Vaccine purchases by countries

When examining month-to-month variations in vaccine sales on country level, we detected minor changes in February 2020 except for a 1159% relative increase in Pakistan. Relative to the same months in 2019, the shift in the vaccine sales trends appeared in March 2020, varying between a relative drop of 70% to a rise of 343%. It persisted through April 2020, with more countries experiencing relative plunges in vaccine sales up to 200% (online supplemental figure 2). Further investigations revealed that the highest vaccine sales escalations in those periods correspond to an oversupply of rabies vaccine to Pakistan in February 2020, and Hib vaccine to Central America in March and April 2020.

Discussion

Main findings

COVID-19 had a significant impact on economies and healthcare systems worldwide. We found that shortly after the COVID-19 pandemic declaration, vaccine sales plummeted globally by over 33% from March to April 2020. However, the vaccine sales interruptions recovered at a differential rate across economies. Between April 2020 and August 2020, HICs experienced a significant decrease of 20.6% in overall vaccine sales, in contrast with a 10.7% significant increase across LMICs, relative to the same period in 2019. At the same time as showing these impacts, our study also highlights the consistent disparities in per capita vaccine purchases before and during the COVID-19 pandemic. Between August 2014 and August 2020, the monthly per capita vaccine sales in HICs were, on average, at least four times higher than in LMICs and nearly three times higher than in UMICs.

Abrupt reductions in global vaccine sales shortly after the COVID-19 pandemic declaration

Our findings demonstrate an abrupt reduction of global vaccines sales in April 2020 relative to March 2020, reflecting the moderate to severe disruptions or complete suspension of immunisation programmes and services reported by half of the countries worldwide.7 The changes to vaccination programmes resulted in inaccurate forecasting plans and inefficient procurement strategies by countries,16 which have further strained manufacturers’ capacity alongside shortages in drug inventories of active pharmaceutical ingredients.27 Beyond government-imposed lockdowns, flight cancellations and countries’ trade restrictions have severely constrained vaccine production, shipments and their timely delivery, as reported by UNICEF, one of the world’s largest procurers of vaccines.9 16

Market recovery

Our study shows that vaccine sales interruptions recovered disproportionately across economies between April and August 2020, with over a 10% increase in vaccine sales across LMICs compared with an over 20% decrease across HICs. This could be linked to differences in the procurement modalities of vaccines, financing of vaccines programmes, and vaccine deployment and administration across economies. Low- and middle-income countries tend to finance their vaccine programmes through national healthcare spending, Gavi and other development partners to cover vaccines, supply chains and service delivery.28 In contrast, higher income countries finance their vaccination programmes through their national healthcare budgets.29 Shortly after the pandemic declaration, significant human and financial resources devoted to vaccinations were diverted to respond to the unprecedented COVID-19 healthcare needs in HICs.9 The repurposed funds reallocated to the pandemic response may explain the relative reduction in vaccine sales across HICs.

While the picture may seem broad, our analysis revealed distinct patterns in vaccine sales for routine, vaccine-preventable diseases and travel vaccines in the post-pandemic period. Although the severity of the impact of COVID-19 has varied across economies, the decreases in demand for vaccines were seen across HICs, reflecting the alteration to routine and travel-related immunisation services. Emerging evidence shows reductions in the administration rates of routine vaccines and primary care visits during initial lockdown measures in countries such as France, Spain, the USA and the UK.12 Furthermore, by May 2020, all destinations worldwide have imposed some form of COVID-19-related travel restrictions, with 163 countries completely closing their borders for international tourism.30 This could explain the large decreases in the sales of yellow fever vaccines, legally required to enter areas in Africa, Central and South America. This is also compounded by declines in the sales of travel-recommended vaccines such as typhoid, rabies, hepatitis A and meningococcal vaccines, which administration depends on age, health and destination.31 32

COVID-19 was also challenging for lower income countries with a young demographic profile at a higher risk of experiencing vaccine-preventable outbreaks. To avoid another public health emergency amid the COVID-19 pandemic, the WHO and UNICEF issued new guidance on sustaining newborn routine vaccination programmes and temporarily suspending mass vaccination campaigns unless infection control measures are adequately implemented.33 In our analysis, the relative increase in BCG vaccine sales in LMICs may reflect the sustainability of newborn immunisation services as an essential health service in these settings. Our findings also revealed distinct drops in vaccine sales, particularly with vaccines requiring multiple doses to complete the vaccination series such as hepatitis B and measles in HICs and LMICs, or vaccine-preventable diseases such as HPV in LMICs. These regressing trends reflect the interruptions or delays in childhood routine vaccination or the suspension of community-based immunisation campaign strategies. The 2020 estimates of national immunisation coverage data, the first published report describing the global service disruptions due to COVID-19, support our findings by demonstrating reductions in the coverage of these vaccines.8 More particularly, the report highlights declines in hepatitis B coverage rates among children aged 1 year old in HICs and LMICs, along with a more severe drop of HPV vaccine coverage in LMICs.8 In addition, coverage of the first dose of measles dropped globally to 84% in 2020, reaching the lowest level since 2010,8 and the COVID-19-related disruptions contributed to the surge of measles outbreaks in at least 18 countries.34 35

Strengths and limitations

Our study should be interpreted within the context of the first wave of the COVID-19 pandemic. A key potential limitation to our study is inherent to its large-scale ecological nature. The governments’ response to the evolving COVID-19 pandemic has manifested in a myriad of public health orders and varying degrees of restrictions on population mobility and borders that were exceptional to each country.36 Variability is likely to exist within a country and among countries grouped under one defined economy. Another limitation of this study is that none of the individual countries for which data were available fell under the low-income countries category. The observed changes in vaccine sales across economies do not necessarily mirror the consumption of vaccines. Nonetheless, supply constraints are an essential aspect of the health system that could limit service uptake.37 Results from our study can inform the need for additional research to investigate why particular vaccine supply chains were more resilient during a global emergency when contrasted with the cascade of lockdown measures. Moreover, we have not explored the geopolitics and global architecture behind vaccine procurement to further understand the discrepancies in per capita vaccine sales across economies. Further research investigating vaccine procurement modalities and their funding schemes in relation to immunisation coverage gaps is crucial to explain the unequal distribution of vaccines.

Our study had multiple strengths. First, we leveraged the use of the IQVIA MIDAS dataset that provides real-world data on vaccine sales across its market coverage spanning over all continents and across three different economies. We harnessed the value of the MIDAS administrative data that are often used and validated to present a global overview of vaccine sales when such data are sparse. Although we focused on purchases as the driving element of vaccines supply, such evidence remains the best information currently available during a period of unprecedented shifts in drug supply and demand to uncover some of these nuanced trends.

Conclusion

In the context of the rapidly evolving nature of the COVID-19 pandemic and emerging disease outbreaks, this study provides valuable data on the discrepancies of vaccine sales over time and across country-income groups, thus contributing to a timely gap in the literature concerning COVID-19-induced disruptions to vaccines. This analysis should be repeated in the future to monitor changes in per capita vaccine sales, and action is critical to support adequate and equitable distribution of vaccines worldwide. Finally, to mitigate the long-term impact of the first pandemic wave, health system planners need to mobilise resources to intensify catch-up immunisation services and regenerate community demand to avoid the resurgence of vaccine-preventable diseases and close immunisation gaps.

Data availability statement

Data may be obtained from a third party and are not publicly available. Data can be obtained through IQVIA.

Ethics statements

Patient consent for publication

Ethics approval

Ethical approval was granted by the University of Pittsburgh Institutional Review Board (Ref. STUDY21060160).

References

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Handling editor Seye Abimbola

Twitter @Zeitouny_S, @SUDAmonas, @myclaw, @Mina__T

Contributors SZ, KJS, MRL, MT conceived and designed the study. KM, SZ conducted the statistical analysis. SZ analyzed the data and drafted the manuscript. KJS, MRL, MT reviewed the draft. KJS, MRL, MT provided administrative, technical, or material support. MT supervised the study. All authors had full access to all of the data (including statistical reports and tables) in the study and take responsibility for the integrity of the data and the accuracy of the data analysis. All authors contributed to revisions of the text and approved the final version of the manuscript. SZ is the guarantor. The corresponding author attests that all listed authors meet authorship criteria and that no others meeting the criteria have been omitted.

Funding The authors have not declared a specific grant for this research from any funding agency in the public, commercial or not-for-profit sectors.

Disclaimer The content is solely the responsibility of the authors and does not necessarily represent the official views of the Department of Veterans Affairs, the US government, or of IQVIA, or any of its affiliated entities. The statements, findings, conclusions, views, and opinions contained and expressed in this publication are based in part on data obtained under license from IQVIA as part of the IQVIA Institute’s Human Data Science Research Collaborative.

Map disclaimer The inclusion of any map (including the depiction of any boundaries therein), or of any geographic or locational reference, does not imply the expression of any opinion whatsoever on the part of BMJ concerning the legal status of any country, territory, jurisdiction or area or of its authorities. Any such expression remains solely that of the relevant source and is not endorsed by BMJ. Maps are provided without any warranty of any kind, either express or implied.

Competing interests MRL received salary support through a Canada Research Chair. The other authors have disclosed no conflicts of interest.

Provenance and peer review Not commissioned; externally peer reviewed.

Supplemental material This content has been supplied by the author(s). It has not been vetted by BMJ Publishing Group Limited (BMJ) and may not have been peer-reviewed. Any opinions or recommendations discussed are solely those of the author(s) and are not endorsed by BMJ. BMJ disclaims all liability and responsibility arising from any reliance placed on the content. Where the content includes any translated material, BMJ does not warrant the accuracy and reliability of the translations (including but not limited to local regulations, clinical guidelines, terminology, drug names and drug dosages), and is not responsible for any error and/or omissions arising from translation and adaptation or otherwise.