Article Text

Abstract

The world faces multiple health financing challenges as the global health burden evolves. Countries have set an ambitious health policy agenda for the next 15 years with prioritisation of universal health coverage under the Sustainable Development Goals. The scale of investment needed for equitable access to health services means global health is one of the key economic opportunities for decades to come. New financing partnerships with the private sector are vital. The aim of this study is to unlock additional financing sources, acknowledging the imperative to link financial returns to the providers of capital, and create profitable, sustainable financing structures. This paper outlines the global health investment opportunity exploring intersections of financial and health sector interests, and the role investment in health can play in economic development. Considering increasing demand for impact investments, the paper explores responsible financing initiatives and expansion of the global movement for sustainable capital markets. Adding an explicit health component (H) to the Environmental, Social and Governance (ESG) investment criteria, creating the ESG+H initiative, could serve as catalyst for the inclusion of health criteria into mainstream financial actors’ business practices and investment objectives. The conclusion finds that health considerations directly impact profitability of the firm and therefore should be incorporated into financial analysis. Positive assessment of health impact, at a broad societal or environmental level, as well as for a firm’s employees can become a value enhancing competitive advantage. An ESG+H framework could incorporate this into mainstream financial decision-making and into scalable investment products.

- health economics

- public health

- health systems

This is an open access article distributed under the terms of the Creative Commons Attribution-NonCommercial IGO License (CC BY-NC 3.0 IGO), which permits use, distribution,and reproduction for non-commercial purposes in any medium, provided the original work is properly cited. In any reproduction of this article there should not be any suggestion that WHO or this article endorse any specific organization or products. The use of the WHO logo is not permitted. This notice should be preserved along with the article’s original URL. See:https://creativecommons.org/licenses/by-nc/3.0/igo

Statistics from Altmetric.com

Key questions

What is already known?

The global health burden is evolving and health financing is therefore becoming more challenging.

Prioritisation of universal health coverage under the Sustainable Development Goals means the scale of investment needed is a key economic opportunity for decades to come.

New partnerships and financing structures with the private sector will be vital.

What are the new findings?

Investment in health supports economic development and global health investment is a large opportunity.

Private sector funders need to see financial return linked to the providers of capital and therefore need new structures which can make this link.

Health considerations directly impact profitability of the firm and therefore should be incorporated into financial analysis.

Positive assessment of health impact, at a broad societal or environmental level, as well as for a firm’s employees can become a value enhancing competitive advantage.

What do the new findings imply?

Adding health investment to responsible financing initiatives and expanding the global movement for sustainable capital markets could provide sustainable and scalable opportunities to develop the intersection between financial and health sector interests.

Adding an explicit health component (H) to the Environmental, Social and Governance (ESG) investment criteria, creating the ESG+H initiative, could serve as catalyst for the inclusion of health criteria into mainstream financial actors’ business practices and investment objectives.

Expanding these responsible investment structures to health could incorporate global health financing needs into mainstream financial decision-making and into scalable investment products.

Introduction

The world presents multiple health challenges as the global health burden evolves, and the price of innovation in health treatment continues to rise. Government budgets are under increasing pressure, savings rates are challenged and public and private sectors wonder how healthcare costs can be financed going forward especially with expansion of universal health coverage (UHC).

Financial sector actors, banks and investors from the asset management and insurance worlds have a key role in the ongoing provision of long-term financing. Critical issues are scalability and the ability to link potential financial returns to risk takers, that is, providers of capital. This paper outlines key areas of mutual interest and provides routes to new investment opportunities drawing on experiences from existing areas of responsible financing.

The global health investment opportunity

Under the Sustainable Development Goals (SDG), countries have set themselves an ambitious health policy agenda for the next 15 years. It ranges from reducing the burden of reproductive, maternal, newborn and child heath, to attaining UHC, to the growing chronic problem of non-communicable diseases (NCD).1 These goals will require sustained and increased investments at country level, and continuous support from the entire global community, in a situation of constrained public budgets.

Health constitutes a major economic force in high-income countries and emerging economies alike. In 2013, total global health expenditure amounted to $7.28 trillion.i In Germany, the health sector constituted 11.2% of the country’s gross domestic product (GDP) in 2013 growing at 3.5% per annum, significantly above the rate for the economy as a whole. Chinese health spending amounted to $511.3 billion, 5.4% of the entire economy2 in 2013, projected to rise at an annual rate of 11.8% until 2018. India—still at comparatively low levels of health spending—is expected to reach almost $200 billion in health expenditures in 2018 with an annual growth rate of more than 12%.3 More than 100 countries have now introduced policies that will help move towards UHC. Increasing coverage in 24 low/middle-income countries since 2006 resulted in 1.5 billion people gaining access to universal health services.4

For low/middle-income countries alone, the World Investment Report 2014 estimates annual health investment needs of $210 billion, and an annual investment gap of some $140 billion per year.5 ,ii Innovation in service delivery through engagement with non-traditional actors such as mobile phone companies in telemedicine, or unconventional screening posts for chronic disease in the community, will provide many opportunities for entrepreneurial ventures and new opportunities for investment.

Breaking down silos: the role of banks in global health

Banks are a powerful partner for better health in a post-2015 world. The scale of market growth and investment volume needed to achieve the SDGs illustrate that global health constitutes one of the key economic opportunities for decades to come. Simultaneously, debate on the SDGs has triggered reinforced efforts to define the role of private sector investment, and its impact on development goals.6 ,iii Global policy leaders show unprecedented willingness to break down silos. United Nations (UN) Secretary General Ban Ki-moon, at the 2015 Addis Ababa Conference Business Forum, urged ‘private sector leaders—including CEOs and institutional investors—to be part of the solution, and to consider new commitments for investment in sustainable development.’7

Financial actors will play multiple roles as lenders, intermediaries and investors across the spectrum of debt instruments and equity investments, from venture capital to public equity markets. On a macroeconomic level, financial development contributes to economic growth, supports innovation, facilitates entrepreneurshipiv and has an immensely important role to play in the welfare of a country. Functionally financial institutions provide credit for investments, liquidity for bridging financial gaps of individuals or companies and risk management services by pooling risks.8

Despite economic opportunity on one side, and political willingness to achieve the development goals on the other, private sector investments in health in low/middle-income countries have not soared. Possible obstacles are numerous: distrust of private sector involvement from health policymakers, short-termism or governance challenges hindering investors from making a long-term commitment. The lack of liquid investment instruments and the difficulty of doing due diligence on new healthcare entrepreneurs have also been highlighted by practitioners.

This paper therefore takes a different approach and identifies possible mutual interests for enhanced cooperation, and analyses potential obstacles and concludes by suggesting steps for future debates.v

Intersection 1: stability and trust

A key condition of stability in both sectors is trust. Investors seek stability in the political and economic environment, an essential criterion for putting capital at risk: ‘The ECB defines financial stability as a condition in which the financial system …can withstand shocks without major disruption.’9 In health systems, a breakdown harms underlying financing mechanisms, and medium term, results in worse health outcomes and impaired opportunities for social or private insurance via risk pooling.

Banking crises and health

Over the past 15 years, there were systemic crises in both systems with severe repercussions on populations, on top of an adverse macrolevel environment.10 The burst real estate bubble in the USA left governments the only actors able to restore trust, and avoid bankruptcies of ‘too-big-to-fail’ institutions. Ben Bernanke, US Federal Reserve Chairman, said in 2008: ‘The crisis will end when comprehensive responses by political and financial leaders restore that trust, bringing investors back into the market.’11

In response to rising public debt levels resulting from banking rescues, and economic stimulus packages, many countries implemented fiscal austerity. Economic hardship and spending cuts have significant effects on health systems and population health, and exacerbate existing inequalities in access to health services.

First, rising unemployment brings a higher rate of psychological illness, and a higher suicide rate. Evidence from Spain suggests that the crisis has been associated with significantly above trend suicide rates (especially among men),12 Italy saw an increase of 40% in deaths by suicide of unemployed persons 2008–2010.13 In the USA, the share of adults reporting serious psychological distress increased substantially since 2007, in particular aged 25–44.14 Although this preliminary evidence should be treated with caution, the short-run trend is worrisome.

Second, governments adopted drastic spending cuts to reduce public debt. The European Observatory on Health Systems and Policies, hosted by WHO, reported that since the financial crisis in 2008, public spending on health fell in absolute terms and as a share of total government spending in many countries. While general coverage seemed unaffected, increased user charges reduced equity and efficiency of the systems.15 ,vi Portugal, for example, committed to savings of €670 million in healthcare16 in order to receive financial support from the European Union resulting in increased out-of-pocket payments from citizens.vii Such spending cuts impact the long-term health of a country. Tighter budgets of individuals and families can also lead to a change in nutrition. Evidence from Australia shows that people who experienced financial distress in 2008–2009 had a 20% higher risk of becoming obese than those who did not.17

Health crises and economic instability

Over the last 20 years, several cross-border epidemics have shocked regions of the world. When an outbreak of severe acute respiratory syndrome was detected in Southern China in 2003, the estimated net loss in global GDP amounted to $18 billion.18 Ebola in 2014 caused 11 300 deaths and led to a virtual breakdown of domestic health systems. In Sierra Leone, where almost 4000 people died due to the Ebola virus, the International Monetary Fund (IMF) estimates that GDP fell by 23.9% in 2015 as compared with the previous yearviii and ongoing health needs were neglected through fear: ‘The rumour among mothers is that, if they take the child to the health centre, the child will get Ebola.’19 Besides the catastrophic death toll of epidemics, health crises can severely damage economic systems and have an ongoing negative impact on economic growth and cross-border trade.

Intersection 2: investment and growth potential

Macroeconomic benefits of investments in health

Meanwhile, the macroeconomic case for (development) investments in health is compelling. Larry Summers and 260 other economists argued that ‘Health systems oriented toward UHC […] produce an array of benefits…estimated to be more than ten times greater than costs…in times of crisis, they mitigate the effect of shocks on communities; in times of calm, they foster more cohesive and productive economies.’20 These investments include high pay-off interventions in health such as $3 billion annually on improving surgical capacity, $1.5 billion annually to expand tuberculosis (TB) training, $1 billion annually to expand immunisation coverage of children, and many more.21 The Copenhagen Consensus Center calculated the benefits from investment into fighting TB, malaria and HIV/AIDS. For TB, preventive treatment costing $8 billion every year would deliver a $359 billion benefit through extending productive lifetimes by 20 years.22

Health investments are already attractive for private sector investors

International investors have long been active in the health sector and the global health themes underpinning these investments have generated superior returns over time. This is reflected in the development of stock market indices. Since 2006, the MSCI World Indexix rose by 60%–70% while the healthcare index rose by almost 150% (figure 1). In emerging markets, the index of the overall economy rose by 20%–25%, while healthcare sector equities rose by more than 160% since January 2006x (see figure 2).

Performance of healthcare stocks versus all stocks, global sample.

Performance of healthcare stocks versus all stocks (emerging market sample). The MSCI Emerging Markets Index is a free float-adjusted market capitalisation index that is designed to measure the equity market performance of emerging markets. It represents about 13% of the world market capitalisation. As of November 2015, the MSCI Emerging Markets Index consists of 23 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, Indonesia, India, Korea, Morocco, Mexico, Malaysia, Peru, Philippines, Poland, Qatar, Russia, Thailand, Turkey, Taiwan, United Arab Emirates and South Africa. Important sectors within the MSCI EM/Healthcare Index are pharmaceuticals (70%), healthcare facilities (19%) and healthcare distributors (7%).

Rising incomes, urbanisation and changing preferences contribute to higher demand for quality healthcare.23 Global health spending reached $7.28 trillion in 2013 and is projected to reach $9.3 trillion by 2018, according to the Economist Intelligence Unit.24 Growth is geographically concentrated in emerging economies: in a study by the Boston Consulting Group and the World Economic Forum, total healthcare spending in emerging countries is projected to rise by an average rate of around 10% until 2022 (developed economies: approximately 4% per annum (see figure 3)).25

Healthcare spending over time and by geography. Sources: World Bank, Business Monitor International and BCG. Illustration and calculations from: World Economic Forum (2014). Health Systems Leapfrogging in Emerging Economies. Geneva. Retrieved from http://www3.weforum.org/docs/WEF_HealthSystem_LeapfroggingEmergingEconomies_ProjectPap er_2014.pdf.

While in 2012 only 20% of healthcare spending came from emerging economies, by 2022 this is estimated to reach 33%. As a result, healthcare systems, and the entire health economy in these countries, will undergo dramatic change and the attractiveness of healthcare investments in future will not only be driven by the ‘usual suspects’ such as pharmaceutical companies. For China, the strategy consulting firm Bain and Company estimates that hospitals and other health service providers will account for 40% of the growth in profits by 2020 (followed by pharma firms for generic products and Medtech at approximately 19% and 14%, respectively).26 Another growth market, the digital healthcare sector, is projected to grow dramatically, from $3 billion in 2014 to $110 billion in 2020.27

New investment products are needed to access further growth potential

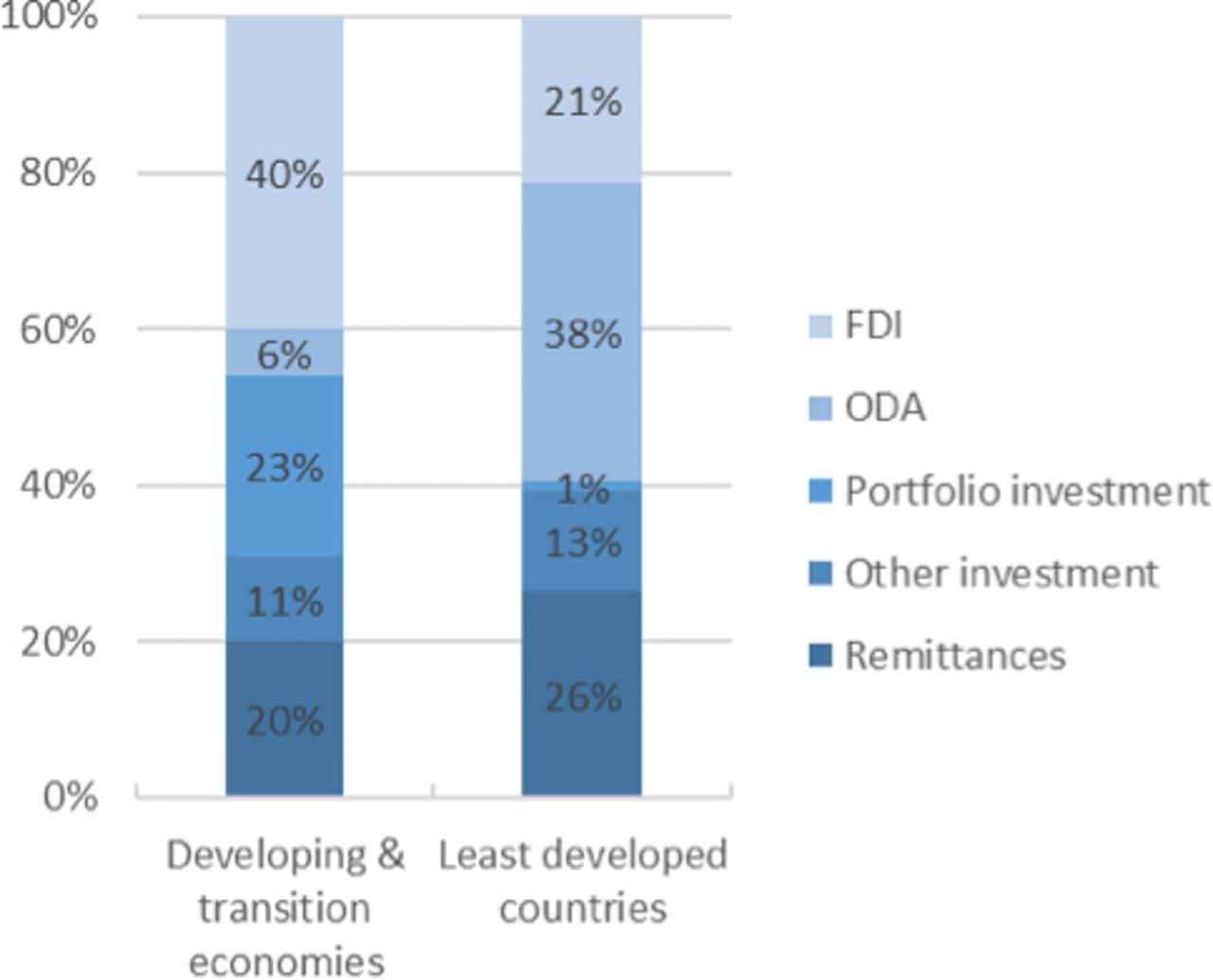

Considering this compelling macroeconomic case and interest from private investors, a key question is how these investments can be channelled into the considerable unfulfilled funding needs of projects supporting health-related SDGs. External development finance in 2012 shows a bias away from the least developed countries (see figure 4). While portfolio investment and foreign direct investment (FDI) combined account for 60% of all external resources flowing into developing and transition economies, the respective number for the least developed countries is only 22%.5

Composition of external sources of development finance, 2012. Sources: Illustration by the authors. Numbers from World Investment Report 2014, p 148. Original data from IMF, UNCAD FDI-TNC-GVC Information system, OECD and World Bank. Notes: (1) Portfolio investment includes, in addition to equity securities and debt securities in the form of bonds and notes, money market instruments and financial derivatives such as options. Excluded are any of the aforementioned instruments included in the categories of direct investment and reserve assets. (2) Other investment is a residual category that includes all financial transactions not covered in direct investment, portfolio investment or reserve assets. (3) Least developed countries include Afghanistan, Angola, Bangladesh, Benin, Bhutan, Burkina Faso, Burundi, Cambodia, the Central African Republic, Chad, the Comoros, the Democratic Republic of the Congo, Djibouti, Equatorial Guinea, Eritrea, Ethiopia, the Gambia, Guinea, Guinea-Bissau, Haiti, Kiribati, the Lao People’s Democratic Republic, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mozambique, Myanmar, Nepal, Niger, Rwanda, Samoa (which, however, graduated from least developed country (LDC) status effective 1 January 2014), São Tomé and Príncipe, Senegal, Sierra Leone, Solomon Islands, Somalia, South Sudan, Sudan, Timor-Leste, Togo, Tuvalu, Uganda, the United Republic of Tanzania, Vanuatu, Yemen and Zambia. FDI, foreign direct investment; ODA, official development assistance.

A bias also exists at sectoral level. While pharmaceutical firms and medical technology companies receive broad attention from investors around the globe,xi other health areas—often the more fundamental ones—have been neglected so far. Evidence from India, for example, showed that a major share of total equity FDI into the healthcare sector ended up in pharmaceuticals. Between 2000 and 2013, 71% went to the pharmaceuticals sector while hospitals and diagnostic centres only received 21% of the FDI equity inflows.28

Banks can play a pivotal role as intermediaries: designing products that allow effective channelling of funds into sustainable projects that improve health in the long run. While so-called impact investors may seek these out, other investment institutions may require greater trading liquidity in collective structures, enabling larger investment flows into the sector via their distribution channels, or via long-term insurance company structures.

Intersection 3: responsibility and investment

Demand for health services and the willingness to invest in personal health increase as incomes rise in emerging economies and institutional changes incentivise people to save for health, to avoid potentially catastrophic out-of-pocket expenditures.

Individuals increasingly saving and investing in their health

Based on how spending patterns evolved in developed economies, the Emerging Market Consumer Survey 2015 of Credit Suisse finds high healthcare growth potential for countries whose GDP per capita ranges from $10 000 to S25 000 and medium for countries whose GDP per capita ranges from $5000 to $10 000.29 Taking estimates for 2019, high growth areas would include countries such as South Africa, China, Mexico, Turkey, Brazil, Russia and Saudi Arabia. Interestingly, despite more people in emerging economies accessing state-funded healthcare in recent years (2011: 26%, 2014: 48%), the share of what people spent on healthcare from their disposable income is stable.29 The desire to invest in personal health can be seen at all socioeconomic levels and across the world. Private health insurers build on this desire and expect growing demand for reimbursement-type health insurance. According to Swiss Re, premiums in emerging markets will grow from roughly $1 trillion in 2013 to $1.48 trillion in 2020 driven in particular by emerging Asia and the Middle East.30

Policies such as national health funds, health savings accounts and other obligatory or voluntary schemes contribute to building up significant savings dedicated for health. In the Singaporean model, for example, the impressive contribution from the Medisave scheme to the national provident fund in 2014 included 3.2 million savings accounts with an average balance of $21 800 totalling $70.5 billion:31 an increase of 500 000 accounts and $13 500 average balance compared with 2000.32

Meanwhile, sovereign wealth funds, with total assets of $7.3 trillion according to the IMF,33 have invested $26 billion into healthcare companies over the last decade, predominantly into pharmaceuticals, with $4 billion also into healthcare providers.xii Recent evidence shows they are prepared to look at innovative financing structures and invest through the cycle for long-term returns.34

More investors ask for sustainability and impact

Conventional investment strategies do not incorporate sustainable health criteria. Indeed, since there are significant growth prospects for companies that endanger health through their expansion in low/middle-income countries—such as soft drinks,xiii packaged foods, alcohol, tobacco35—investors are encouraged to include these into their portfolios.36 The costs to societies are not considered in economic calculations.

Over the past 20 years, the average annual growth rate of the consumed volume of soft drinks in low/middle-income countries was over 5%.37 Between 1960 and 2000, the consumption of cigarettes rose at an annual rate of 4%, with a particular focus in emerging markets. According to WHO figures, tobacco kills around 6 million people every year and in 2030, 80% of the deaths due to tobacco will come from low/middle-income countries. A study by the World Economic Forum highlighted that over the next 20 years, NCDs such as cancer, heart disease and stroke will cost more than US$30 trillion, representing 48% of global GDP in 2010, and push millions of people below the poverty line.38

Banks and asset managers serve a growing group of investors who request a say in which sectors their money is invested. Clients increasingly challenge whether investments into treatment, for example, pharmaceuticals, rather than prevention of the rising burden of lifestyle diseases in emerging economies actually contribute to improved health status.xiv Calls for divestment from companies and sectors that offer harmful products, in favour of more sustainable industries, have been prominent already in climate change-related sectors. As of November 2015, the global initiative ‘go fossil free’ reports that almost 500 institutions have committed to divest from fossil fuel representing $3.4 trillion of assets.39 Transparency initiatives enabling investors to see clear information on companies’ climate footprint, and the emergence of entrepreneurial companies working on clean energy solutions have helped. There has been supportive government legislation and even fiscal incentives in some countries enabling growing investment in this area.

By including a health ethos in their investment decisions, banks can contribute to better health for millions simply by screening for harmful products in their investment portfolios and offering clients a ‘healthier choice’.

Encouraging ‘responsible banking’ strategies

‘Responsible banking’ has gained importance40 as a partial solution. A strong commitment to sustainable development and integration of corporate social responsibility is a core element in business strategy. Importantly, ‘responsible’ not only means compliant with laws and regulations. Principles include good governance, transparent customer relations, positive contributions to the community and environmentally friendly business, while striving for financial health and stability.

Elements of these concepts are already incorporated in strategies of banks. For example, Deutsche Bank committed to a different banking model in 2014. The Corporate Responsible Report 2014 (CSR) report framed the bank’s role: ‘In whatever business we do, wherever we do it, we aim to serve our clients, our people, our investors, and society, whilst supporting the communities in which we serve and sustaining the environment in which we all live.’41

The push towards more responsible business strategies is a crucial element in harnessing banks as true partner for better health. There needs to be ongoing influence from policymakers and the public to drive this into every day practice, and mainstream products.

Considering health effects in investment decisions: ESG+H

Health has not yet been included into many CSR efforts. ESG investments, including Environmental, Social and Governance criteria, have become increasingly important, hailed in 2013 by Deutsche Bank as a ‘breath of fresh air’ in portfolio investing42 and a means to significantly reduce investment risk.43

The global movement for sustainable capital markets fosters collaboration between investors, regulators and companies to enhance transparency and delivery on ESG criteria. The UN-sponsored sustainable stock exchange initiative now has 15 stock exchanges with published ESG reporting guidance to their members and 23 more committed to this path (out of a total 79 targeted) spanning the world from highly developed, for example, the New York Stock Exchange and Nasdaq, to smaller developing capital markets such as Kazakhstan or Rwanda.44

In recognition of the importance of health investment, an explicit health component (H) could be added to ESG creating the ESG+H initiative. There are several examples that demonstrate how health plays an important role in the profitability of a firm. According to the Global Health Initiative of the World Economic Forum, 72% of companies surveyed reported a negative impact on their business from malaria, with 39% perceiving these impacts to be serious.45 Moreover, a study conducted by the Centers for Disease Control and Prevention found obese men miss, on average, 56% more days compared with ‘normal’ weight men.46

Conclusion

This paper has analysed the investment opportunity in health. Evidence that health conditions directly affect the profitability of the firm demonstrates financiers and investors should incorporate this into their models. Insurance companies who are already experts at including environmental and health risks in their pricing models could provide valuable insights into how to incorporate these measures into other financial sector business models and reporting. In the annual reports of listed companies we already see notices on corporate governance criteria and increasingly on climate or water considerations. Health could also be included, both as a criterion of how well the company looks after its own employees’ health, and also how it impacts health at a broader societal or environmental level through its operations. Positive contributions can become a value-enhancing competitive advantage and investment criterion. An ESG+H framework could bring this to the mainstream. Banking and health have considerable mutual interests (see figure 5).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Mutual interests for Banking and Health - some critical questions to conside.

A second paper will look at precedents from sustainable finance and the climate financing world and explore how these could be adapted for double bottom line health investment.

Supplementary file 1

References

Footnotes

↵ i WHO Health Expenditure Database. Latest observation 2013.

↵ ii For an overview of different estimates, see also http://www.unsdsn.org/resources/publications/sdg-investment-needs/.

↵ v This report builds on the results of the informal consultations on ‘Banking for Health’ in February 2015 in Geneva and extends a previous working paper on the links between banking and health. The exchange that happened between the WHO and the banks as well as civil society organisations aimed at fostering the understanding of the opportunities that arise in ‘banking for health’.

↵ vi See for an overview on the Greek case: Simou and Koutsogeorgou.49

↵ vii As a result, payments by citizens for primary care appointments more than doubled (from €2.25 to €5.00) and the cost of emergency visits increased from €3.80 to €10.00 in primary care, and from €9.60 to €20.00 in secondary care.

↵ ix This is designed to measure equity market performance of the global market.

↵ x MSCI indices are provided by MSCI, a US-based stock market index. Indices obtained from www.onvista.de. See for more information the explanation in the figures.

↵ xii Data from Sovereign Wealth Fund Institute cited in: http://blog-imfdirect.imf.org/2015/10/26/sovereign-wealth-funds-in-the-new-era-of-oil/.

↵ xiii Data retrieved from the Forbes Global 2000 list. Calculations by the authors.

↵ xiv See for example an investment promotion brief of Newton Investment Management—an investment arm of BNY Mellon Asset Management: http://www.newton.co.uk/uk-institutional/file/ip-sept-2015-health-care-in-emerging-markets-a-healthy-development/.

Handling editor Seye Abimbola

Contributors IK, RK, CF and NW contributed to this work and have all approved the final version and are held accountable for its content. IK and RK were responsible for the conception and design of this study and analysis and interpretation of data. CF and NW were responsible for design and the acquisition, analysis and interpretation of data and for the final draft.

Funding This study was funded by the World Health Organization.

Disclaimer The author alone are responsible for the views expressed in this publication and they do not necessarily represent the views, decisions or policies of the World Health Organization.

Competing interests None declared.

Patient consent Not required.

Provenance and peer review Commissioned; externally peer reviewed.