Article Text

Abstract

Introduction Migrants are a vulnerable population and could experience various challenges and barriers to accessing health insurance. Health insurance coverage protects migrants from financial loss related to illness and death. We assessed social health insurance (SHI) coverage and its financial protection effect among rural-to-urban internal migrants (IMs) in China.

Methods Data from the ‘2014 National Internal Migrant Dynamic Monitoring Survey’ were used. We categorised 170 904 rural-to-urban IMs according to their SHI status, namely uninsured by SHI, insured by the rural SHI scheme (new rural cooperative medical scheme (NCMS)) or the urban SHI schemes (urban employee-based basic medical insurance (UEBMI)/urban resident-based basic medical insurance (URBMI)), and doubly insured (enrolled in both rural and urban schemes). Financial protection was defined as ‘the percentage of out-of-pocket (OOP) payments for the latest inpatient service during the past 12 months in the total household expenditure’.

Results The uninsured rate of SHI and the NCMS, UEBMI/URBMI and double insurance coverage in rural-to-urban IMs was 17.3% (95% CI 16.9% to 17.7%), 66.6% (66.0% to 67.1%), 22.6% (22.2% to 23.0%) and 5.5% (5.3% to 5.7%), respectively. On average, financial protection indicator among uninsured, only NCMS insured, only URBMI/UEBMI insured and doubly insured participants was 13.3%, 9.2%, 6.2% and 5.8%, respectively (p=0.004). After controlling for confounding factors and adjusting the protection effect of private health insurance, compared with no SHI, the UEBMI/URBMI, the NCMS and double insurance could reduce the average percentage share of OOP payments by 33.9% (95% CI 25.5% to 41.4%), 14.1% (6.6% to 20.9%) and 26.8% (11.0% to 39.7%), respectively.

Conclusion Although rural-to-urban IMs face barriers to accessing SHI schemes, our findings confirm the positive financial protection effect of SHI. Improving availability and portability of health insurance would promote financial protection for IMs, and further facilitate achieving universal health coverage in China and other countries that face migration-related obstacles to achieve universal coverage.

- health insurance

- cross-sectional survey

- health systems

This is an Open Access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/

Statistics from Altmetric.com

Key questions

What is already known about this topic?

Social health insurance schemes are the main focus of efforts to promote access to healthcare and financial protection in low-income and middle-income countries.

Evidence on social health insurance coverage and its financial protection effect is currently scant for rural-to-urban internal migrants in China, which account for about one-fifth of the total population.

What are the new findings?

Rural-to-urban internal migrants face barriers to accessing social health insurance schemes, especially at current residence.

Social health insurance, regardless of the type of scheme, positively protected against the financial burden of inpatient services for rural-to-urban internal migrants. However, the rural scheme had a smaller protection effect than urban schemes.

Recommendations for policy

Qualifying migrants for social health insurance schemes at their current residence and improving portability of health insurance would be important approaches to promote financial protection in health, and facilitate universal health coverage in China and other countries that face emerging migration issues.

Introduction

By the end of 2015, the estimated population of rural-to-urban internal migrants (IMs) in China had reached 277.5 million, accounting for one-fifth of China’s population.1 2 Like many other countries across the world, achieving universal health coverage (UHC) is one of China’s health priorities to ensure all people receive needed quality healthcare without financial hardship. Social health insurance (SHI) has been the primary focus of efforts to promote access to healthcare and to provide financial protection against impoverishing healthcare cost in China and other low-income and middle-income countries.3 4 SHI has made remarkable progress in China since the late 1990s. Similar to many countries that currently have SHI systems,5 China started the reform of national SHI schemes by first introducing an SHI scheme for workers in 1998, which is the urban employee-based basic medical insurance (UEBMI). In 2003, the new rural cooperative medical scheme (NCMS), a form of community-based health insurance, was established and offered cover to rural residents. Later, in 2007, the urban resident-based basic medical insurance (URBMI) scheme for unemployed urban residents was piloted and then scaled up across China. The NCMS and URBMI are mainly subsidised by the local government, while the financing of the UEBMI comes mainly from joint urban employers and employees’ premiums.6 The detailed financing and benefits of the three SHI schemes are summarised in table 1.6–8 By the end of 2015, the Chinese government had successfully provided the three SHI schemes to more than 95% of the population.9

Financing and benefits among three social health insurance schemes

In China, rural-to-urban IMs face a dilemma regarding access to SHI, which was mainly created by the registered permanent residence (hukou in Chinese) system. Rural and urban residents are categorised separately according to their hukou,10 11 and the government financing of the NCMS and the URBMI only targets rural and urban residents, respectively.10 That is without an urban hukou status, the rural-to-urban IM population is largely excluded from accessing the URBMI available only to urban residents, and their eligibility for the UEBMI varies across the country depending on local UEBMI policies. For example, in the China Health and Retirement Longitudinal Study, retired rural-to-urban IMs were more likely to be uninsured (relative risk ratio=1.39, 95% CI 1.24 to 1.57) compared with their local counterparts.12 Another study conducted in the South China’s megacity of Shenzhen found 43.1% of IMs and 12.2% of local residents were uninsured, respectively, and IMs were five times as likely as their urban peers to be uninsured.13 On the other hand, although IMs are eligible for the NCMS, the scheme runs at the county level and encourages enrollees to use designated hospitals within the county. For migrants who use health services outside the NCMS counties, the coinsurance for health services could rise markedly, and they need to pay for health services out-of-pocket (OOP) and afterwards get reimbursed.14 High OOP payments could discourage IMs from seeking care and may lead to impoverishment or even destitution for people with a need for treatment.3

While there is a growing literature assessing SHI schemes among urban or/and rural residents, such as coverage, financial protection and equality of insurance schemes,15–18 only a few studies have been carried out among IMs. Most of the studies among IMs in China have focused on the impact of SHI status on health service utilisation.19–21 Yet little is known about SHI coverage and its financial protection effects among this vulnerable population. Previous studies showed insurance coverage was not significantly associated with OOP payments among IMs.22 23 While the level of OOP payment is indicative of financial protection, it fails to measure the extent to which the cost of medical services accounts for a household’s living budget, and limits the comparison across regions and time. Therefore, WHO suggests using indicators drawn from both medical costs and household expenditure data to monitor financial protection.3 Thus, using data from the 2014 ‘National Internal Migrant Dynamic Monitoring Survey (NIMDMS)’, our study aimed to extend our knowledge of coverage and financial protection in SHI schemes among rural-to-urban IMs in China. We hypothesised that (1) rural-to-urban IMs would have lower health insurance coverage than the national average and would vary by regions, and (2) the financial protection would be stronger among SHI insured rural-to-urban IMs than their uninsured counterparts and the relative degree of protection would vary by schemes.

Methods

Data resource

The current study used data from the NIMDMS, collected in May 2014. The NIMDMS is a nationwide cross-sectional study aimed to be representative of IMs in mainland China, and is funded and organised by the National Health and Family Planning Commission of China (NPFPC) yearly since 2009, with the fieldwork undertaken by local Health and Family Planning Commissions.24 We chose the 2014 NIMDMS data because the NIMDMS changed survey topics every year, and variables related to SHI coverage and financial protection were only included in the 2014 questionnaire. The 2014 NIMDMS data (http://hdl.handle.net/11620/10725) are publicly available to authorised researchers who have been permitted by the NPFPC, and we received the permission.

Study participants and sampling

The 2014 NIMDMS included IMs aged 15–59 years old who had lived in the study sites for at least 1 month prior to the survey. IMs are defined as individuals who do not have hukou in the study sites, excluding people migrating for study/training purposes, tourism and medical care.24 IMs with urban hukou were excluded for the analysis in this study.

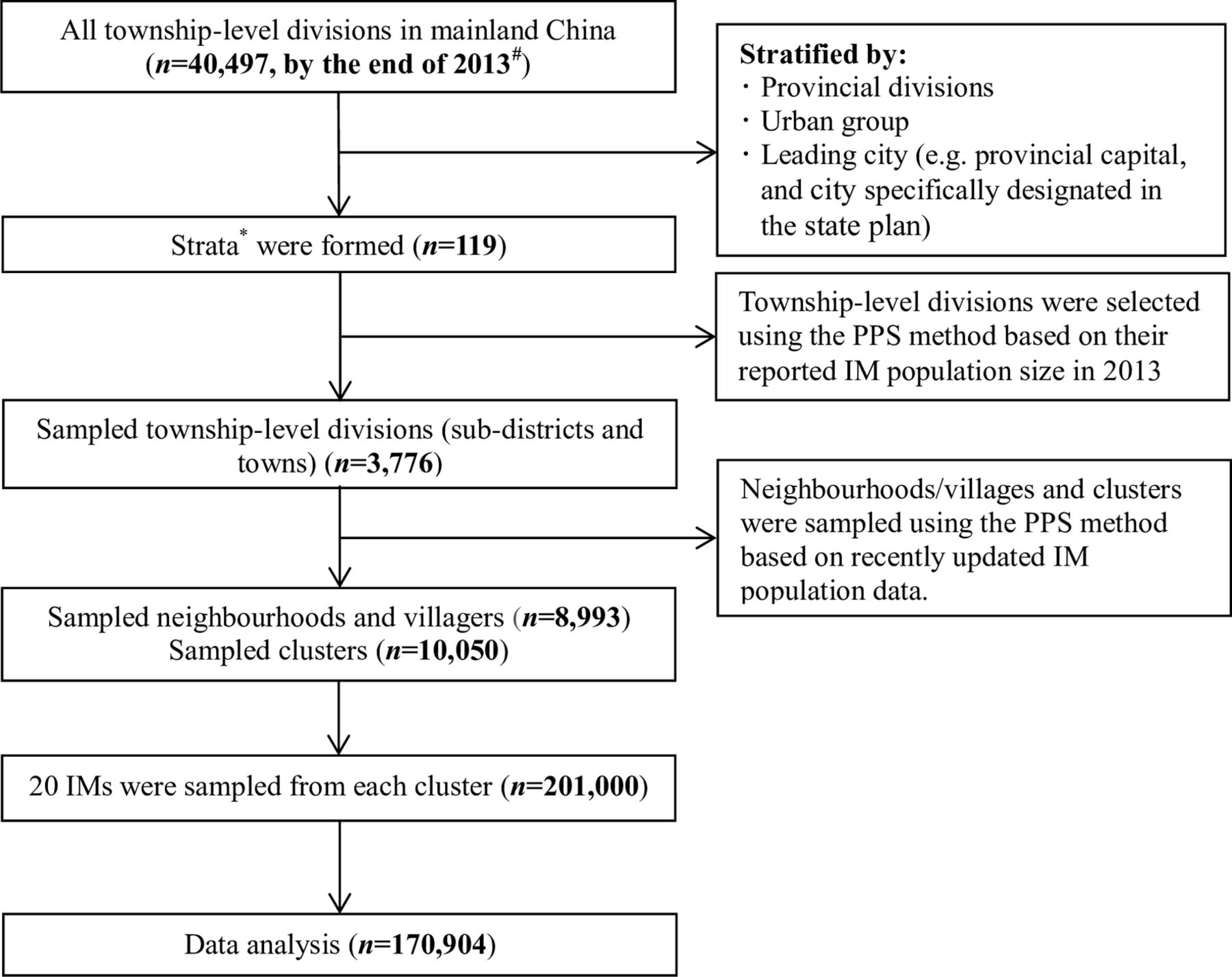

The 2014 NIMDMS planned to investigate 201 000 IMs in all provinces in mainland China. The survey was based on a stratified three-stage sampling design (figure 1).24 25 There were a total of 119 strata in mainland China, stratified by province, urban group and leading city, such as provincial capital and city specifically designated in the state plan (see online supplementary table S1). Sample selection was then carried out independently within each stratum. At the first stage, 3776 township-level divisions were selected with probability proportional to size26 (the number of IMs in 2003). At the second stage, a total of 8993 urban neighbourhoods and rural villages with 10 050 clusters were selected from sampled township-level divisions by probability proportional to size (the number of IMs in 2014). At the third and final stages, 20 eligible IMs were selected in each sampled cluster by the following steps. First, all eligible IMs in each sampled neighbourhood/village were enumerated, and divided into several groups with a group size of around 150 IMs. Second, one or more clusters were randomly sampled among all groups. Then, within each cluster, a simple random sample of 20 IMs was chosen. If a selected migrant came from the same family as another participant or was not able to be contacted, or refused to participate, then the next migrant listed in the sampling frame, with same sex and similar age and duration of residence, was selected for replacement. Face-to-face interviews were conducted via home visits. Interviewers received standardised training by the NPFPC, and quality control was implemented in data collection and input. More details about the technical aspects of the survey are available.24

Supplementary file 1

Sampling flow chart. #Data source: China statistical yearbook 2014. IM, internal migrants; PPS, probability proportional to size.

Measures

SHI schemes status

Respondents were asked if they were participating in the NCMS, UEBMI or URBMI (yes/no). Based on the responses, study participants’ SHI schemes status were further categorised as the following:

Uninsured by SHI: The respondents did not participate in any SHI scheme.

Only NCMS insured: The respondents participated in the NCMS only. Rural-to-urban IMs are eligible for the NCMS in their county of origin.

Only urban basic medical insurance schemes (UEBMI/URBMI) insured: The respondents participated in either the UEBMI or URBMI. The two insurance schemes were combined because they cover mutually exclusive population (employed vs unemployed population), and only 3.7% of the participants reported participation in the URBMI.

Doubly insured: IMs participated in rural (NCMS) and urban (UEBMI/URBMI) schemes at the same time. Due to independent systems for rural and urban SHI schemes, migrant workers who had participated in the NCMS could also enrol in the UEBMI.

Financial protection

To measure the relative degree of financial protection effects across SHI schemes status, we used one key indicator—the percentage of OOP payments for the latest inpatient service during the past 12 months in the total household expenditure—and other secondary indicators (table 2).

Definitions of measurement variables on financial protection of SHI

As recommended by the WHO, the monitoring of financial protection is typically based on indicators generated from both OOP payments and household expenditure. For example, as the most common indicator, catastrophic health expenditure is defined as OOP payments for healthcare exceeding a portion of a household’s expenditure, that is, 25% of total expenditure.3 However, the 2014 NIMDMS data only included respondents’ OOP payments for the latest inpatient service during the past 12 months. We, therefore, calculated the relative degree of financial protection as the the percentage of OOP payments for the latest inpatient service during the past 12 months in the total household expenditure as a surrogate measure of catastrophic health expenditure. Moreover, to adjust the financial protection effect of private health insurance (86 participants got reimbursements), we added reimbursements from private health insurance into the participants’ OOP payments. Our suggested method is supported by the fact that inpatient services’ costs are the main source of OOP payments among IMs in China, with costs of inpatient services accounting for around 75% of annual medical expenditures among IMs,27 and only 5.9% of the study participants have multiple inpatient stays.

Inpatient services utilisation

Respondents were asked whether they used inpatient services prescribed by doctors during the past 12 months (yes/no), what level of health facilities they accessed at the time of the latest inpatient service use (county/district hospitals and below, or municipal hospitals and above) and where were the health facilities (within county of origin, or out of county of origin).

Confounding factors

Respondents’ demographics that were associated with individuals’ willingness to participate in and/or benefited from health insurance schemes were included, such as age, sex, monthly income, annual household expenditure, marital status, education level, employment status, duration of migration, whether migrating with families, household size and region of sending provinces (Western/Central/Eastern China).14 22 28 In the NIMDMS, the household was defined as an economic unit in which a group of persons live and eat their meals together, excluding left-behind spouses and children in rural areas.24

Statistical analysis

Analyses were conducted using IBM SPSS Statistics V.21.0. Descriptive statistics including the mean, SD, median, IQR, frequency and proportion were used to summarise the demographics, inpatient services utilisation and financial protection among study participants with different SHI schemes status, and differences among statuses by study variables were assessed by one-way analysis of variance for continuous variables or the χ2 test for categorical variables. In addition, Fisher’s least significant different test was used to further compare the subgroup differences on financial protection indicators that were found significant on one-way analysis of variance (p<0.05).

Population weighted uninsured rate of SHI, the NCMS, UEBMI/URBMI and double insurance coverage and 95% CIs were estimated based on a survey weight that ranged from 0.01 to 17.57.24 The survey weight was composed of three parts of weight to reduce biases due to unequal probabilities, non-response and non-coverage of the population.29 In addition, the QGIS V.2.18.10 software was used to translate the UEBMI/URBMI coverage and uninsured rate by current provinces of residence and the NCMS coverage by sending provinces into maps.

The financial protection effect of SHI schemes among participants who used inpatient services in the past 12 months was assessed by three-level generalised linear mixed models (GLMMs). IMs were the first level who nested within current counties/districts of residence (level 2) and further nested within current cities of residence (level 3). First, bivariate three-level GLMMs with log link were used to analyse simple associations between the financial protection effect and participants’ SHI status, indicators of inpatient services utilisation and confounding factors. Second, a multivariate three-level GLMM with log link was built to assess the association between health insurance status and the financial protection effect, while controlling for all variables that were found significant on bivariate GLMMs (p<0.10), and percentage share of total medical expenditures on the latest inpatient service.

Results

A total of 200 937 IMs were recruited in the 2014 NIMDMS, and 170 904 (85.1%) rural-to-urban IMs were included in this study with a mean age of 33.4 (SD=9.4) years (table 3). There were 100 201 male participants (58.1%), and 87.8% of the participants (n=150 031) were either employed or employers.

Characteristics of internal migrants in the 2014 National Internal Migrant Dynamic Monitoring Survey (n=170 904)

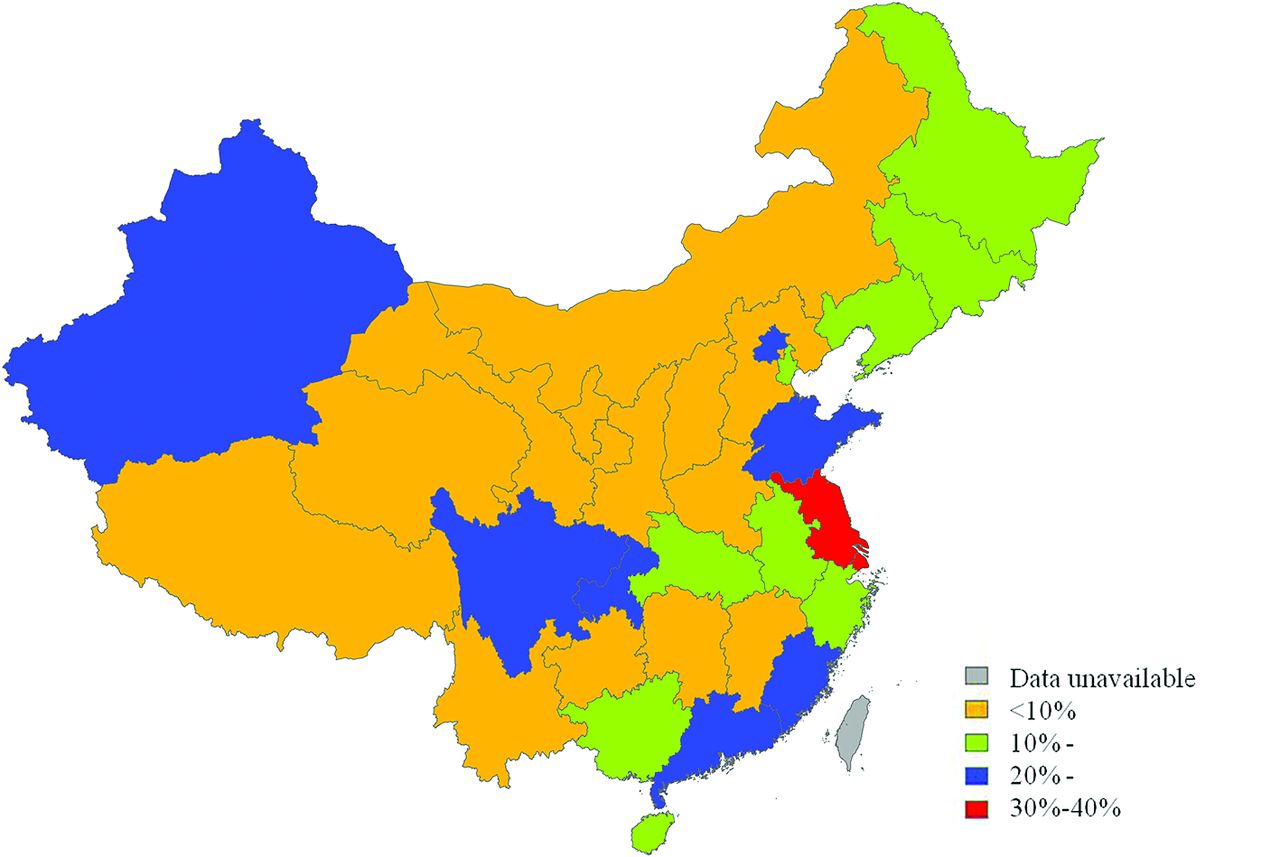

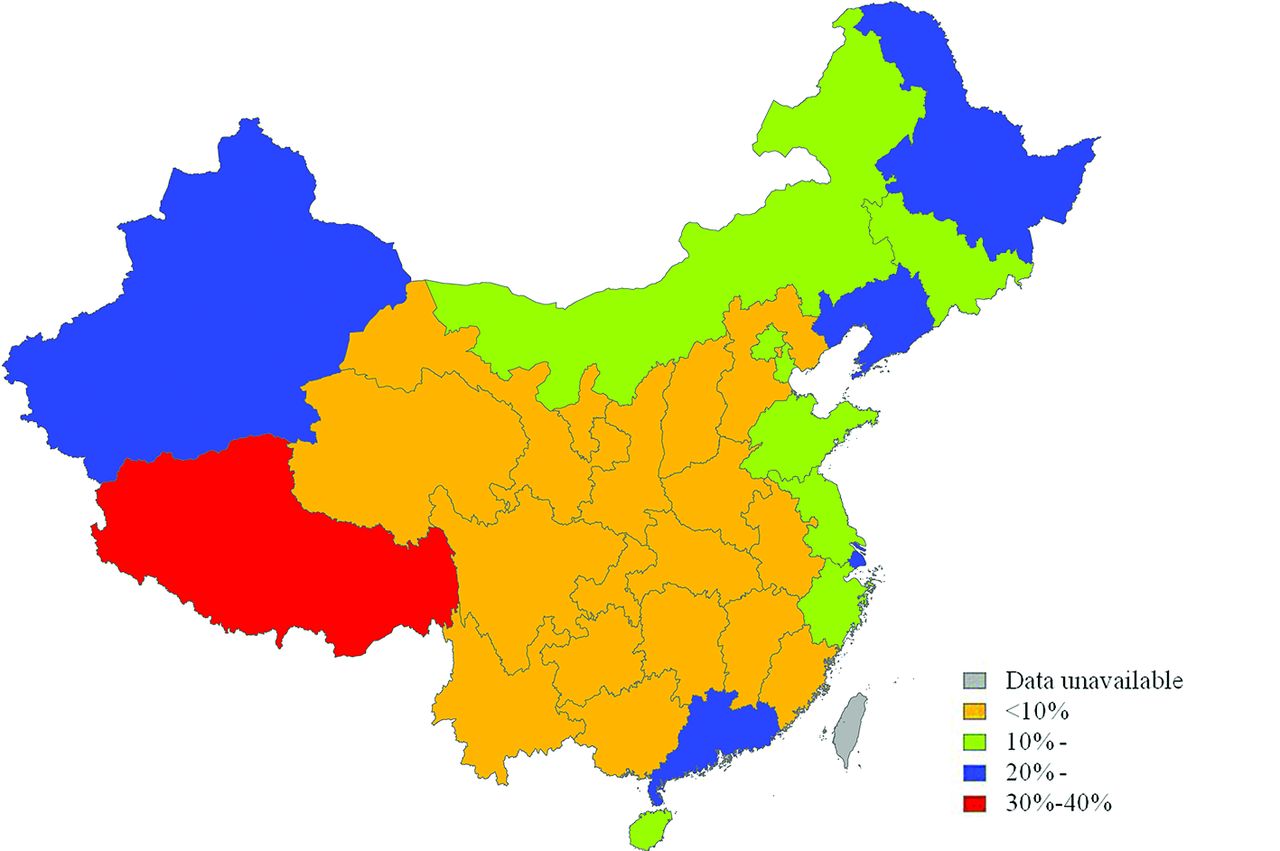

Based on self-reported data (table 4), 23 539 out of 170 904 participants had not enrolled in any SHI scheme (weighted uninsured rate: 17.3%, 95% CI 16.9% to 17.7%), 119 997 participants had enrolled in the NCMS only, 21 272 participants had enrolled in the UEBMI/URBMI only, and 6096 participants were doubly insured (weighted coverage: 5.5%, 95% CI 5.3% to 5.7%). Therefore, 126 093 (119 997+6096) participants had enrolled in the NCMS (weighted coverage: 66.6% (66.0% to 67.1%)), and 27 368 (21 272+6096) participants had enrolled in the UEBMI/URBMI (weighted coverage: 22.6% (22.2% to 23.0%)). It is worth noting that SHI schemes coverage in rural-to-urban IMs varied across mainland China. Overall, rural-to-urban IMs living in Central China had the lowest uninsured rate of SHI (mean=6.9% (SD=2.2%)), compared with IMs living in Eastern (17.3% (5.8%)) and Western China (10.9% (8.7%)) (figure 2). The NCMS coverage in participants from Western (74.1% (12.2%)) and Central China (77.8% (4.4%)) was higher than Eastern China (66.8% (6.3%)) (figure 3). However, Eastern China had the highest URBMI/UEBMI coverage (19.5% (8.8%)) among the three regions (9.0% for Central China, SD=4.1%; 11.3% for Western China, SD=8.0%) (figure 4).

Uninsured rate of social health insurance among 170 904 rural-to-urban internal migrants by current province of residence in China, 2014.

The new rural cooperative medical scheme coverage in 170 904 rural-to-urban internal migrants by sending province in China, 2014.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The urban employee-based/resident-based basic medical insurance scheme coverage in 170 904 rural-to-urban internal migrants by current province of residence in China, 2014.

Inpatient services utilisation and financial protection effect of SHI schemes among internal migrants in the 2014 National Internal Migrant Dynamic Monitoring Survey (n=170 904)

Table 4 shows 5378 (3.1%) participants had used inpatient services during the past 12 months, 317 of them had multiple inpatient stays, and 86 of them got reimbursements from private health insurance. The percentage share of OOP payments for the latest inpatient service was 13.3% (IQR: 8.0%–22.2%), 9.2% (4.8%–18.1%), 6.2% (2.6%–12.8%) and 5.8% (2.4%–13.6%) among participants without SHI, only covered by NCMS, only covered by URBMI/UEBMI and had both insurances, respectively (p=0.004). The average effective SHI reimbursement ratio was 24.0% (0.0%–50.0%), 56.3% (28.1%–75.0%) and 50.0% (25.8%–73.6%) among participants enrolled in only NCMS, only URBMI/UEBMI and both insurances, respectively (p<0.001).

Table 5 reveals that the average percentage share of OOP payments for the latest inpatient service among individuals who only participated in the NCMS and only participated in the URBMI/UEBMI was 6.2% (p=0.009) and 11.1% (p<0.001) lower than their counterparts who had no SHI. The average percentage share of OOP payments among participants who were only insured by the NCMS was 4.9% higher than that of the URBMI/UEBMI insured individuals (p=0.034). There was no statistically significant difference between the doubly insured and SHI uninsured groups. Furthermore, differences in effective SHI reimbursement ratio were statistically significant between any two groups, except the difference between the doubly insured and the URBMI/UEBMI insured participants.

Post-hoc comparisons on financial protection indicators among four groups with different SHI status: results of Fisher’s least significant difference tests

With a multivariate three-level GLMM with log link (table 6), we detected the positive financial protection effect of SHI schemes among rural-to-urban IMs. After adjusting the protection effect of private health insurance and controlling for confounding factors, compared with participants without SHI, the average percentage share of OOP payments for the latest inpatient service among participants only covered by the URBMI/UEBMI, only covered by the NCMS and covered by both schemes increased by a factor of 0.661 (95% CI 0.586 to 0.745), 0.859 (0.791 to 0.934) and 0.732 (0.603 to 0.890), respectively. In other words, compared with no SHI, the UEBMI/URBMI could reduce the average percentage share of OOP payments for the latest inpatient service by 33.9% (95% CI 25.5% to 41.4%), and the NCMS and double insurance could reduce the percentage by 14.1% (6.6% to 20.9%) and 26.8% (11.0% to 39.7%), respectively.

SHI financial protection effects among internal migrants who used inpatient services in the 2014 National Internal Migrant Dynamic Monitoring Survey: results of three-level GLMMs with log link (n=5378)

Discussion

Ensuring access to health insurance and financial protection in health for migrants is a global public health concern.30 China, with a sizeable migrant population from diverse socioeconomic and cultural backgrounds, provides a great opportunity to assess the financial protection effect of SHI. Moreover, by providing two different types of SHI scheme for many IMs, including the UEBMI, a traditional form of SHI in which employees and employers pay via contributions based on salaries, and the NCMS, a form of community-based health insurance, China can provide lessons for many counties facing migration-related obstacles to achieve universal coverage.

Our study provides evidence that rural-to-urban IMs face barriers to accessing SHI in China and the barrier varies by schemes. Specifically, we found that rural-to-urban IMs had 12.3% higher uninsured rate of SHI than the national average (17.3% vs <5%),9 more than 72.4% lower UEBMI/URBMI coverage than urban residents (22.6% vs >95%),9 and 32.3% lower NCMS coverage than rural residents (66.6% vs 98.9%2). Worldwide, many countries face the challenge of financing healthcare for migrants. Although sporadic, there are innovative approaches to enhancing UHC among migrants. For example, as a regional hub for migrants in Asia, Thailand has introduced health insurance programmes for migrants since 1997, including the compulsory migrant health insurance targeting registered migrant workers, and the voluntary migrant health insurance scheme for documented and undocumented migrants who are not covered by the mandatory scheme.31 32 Both schemes cover migrant-friendly comprehensive healthcare services that are similar to the Thai UHC scheme for citizens. Despite these efforts, the population coverage was still suboptimal. By 2015, the two schemes covered around 1.6 out of 3.5 million estimated migrants in Thailand. Poor portability of the schemes, the voluntary nature of migrant health insurance and migrants’ illegal status are key barriers to enrolment. In Europe, providing healthcare for immigrants, particularly undocumented migrants, is also a matter of concern and challenge. A small number of European countries provide full access to healthcare to migrants under specified conditions, including France, Switzerland, the Netherlands, Spain and Portugal. For example, in France, the UHC Act, and the state and home medical assistance provide insurance coverage and full access to public healthcare to migrants. In the Netherlands, compulsory private insurance covers migrants who pay income tax, and the government covers undocumented migrants’ necessary medical expenditures. In Switzerland, undocumented migrants are obliged to purchase statutorily private health insurance. However, implementation challenges still exist in these countries. For instance, complex application process, costly premium, inadequate benefits and uneven implementation of policies across regions impede migrants’ inclusion.33 Moreover, to qualify Chinese IMs for schemes at their current residence, there is an urgent need to implement and deepen the reform of hukou system to eliminate hukou-related obstacles to access health insurance.34 Further research on the economic impact of the current and approaching schemes will be needed.

Additionally, geographical disparities in the coverage of SHI, especially the urban schemes, existed in China. Eastern China has higher coverage of the UEBMI/URBMI but lower coverage of the NCMS than Western and Central China. One explanation is that, as the primary destination of IMs in China, Eastern China could have more migrant-sensitive health systems compared with other regions. For instance, in some Eastern cities, local governments developed special projects to recruit migrant workers into the UEBMI, and integrated the NCMS and URBMI into one scheme to eliminate the hukou barrier to accessing health insurance.12 14 Another possible explanation is that, in Eastern China, more IMs who did labour contract needed jobs than their peers in Western and Central regions,1 which could increase enrolment of IMs into the UEBMI. Similarly, in Vietnam, rural-to-urban IMs who worked in industrial zones had higher insurance coverage than IMs who worked without labour contracts or are self-employed.35 Regarding the relative optimal NCMS coverage in Western and Central China, it may be mainly due to the Chinese government’s financing scheme to encourage the NCMS enrolment in these poor regions.36 For example, in 2014, the central government paid for US$32 and US$26 out of US$47 government subsidies in Western and Central China, respectively.37 In conclusion, developing migrant-sensitive health systems and tailored health insurance policy would be key approaches to reduce geographical disparities in SHI coverage among this vulnerable population.

We also found that after adjusting the protection effect of private health insurance and controlling for confounding factors, regardless of the type of scheme, SHI insured participants received greater protection against the financial burden of inpatient services than uninsured participants. Our study provides new findings opposite to the previous studies conducted among IMs in China.22 23 Inconsistent measurements of financial protection and sampling framework (ie, only OOP payments were measured in existing regional studies) and improvement in SHI implementation in China over the years could lead to the differences. Moreover, we pointed that the fragmented SHI system and hukou management in China could weaken the financial protection effect of SHI schemes. For example, the result shows the NCMS had a smaller protection effect than urban schemes. Low effective reimbursement ratio of the NCMS due to the limited portability and the reimbursement payment lag could be a leading explanation. For instance, Qiu et al14 found 65% of IMs did not receive inpatient reimbursements because of not staying in an NCMS designated hospital, and the majority of designated hospitals are within the county. Additionally, under the current NCMS policy, IMs who used health services outside the NCMS counties need to pay for OOP payments at the time of services use and get reimbursed afterwards. The reimbursement payment lag could also increase financial hardship in a short period. Second, according to the ‘salmon bias hypothesis’, many migrants choose to return to home town on being on an illnesses due to limited access to health services, insurance and supports in the receiving areas,38 which could cause delays in seeking health services and further increase treatment costs.39 Moreover, the NCMS sets lower ceiling and higher coinsurance than the UEBMI/URBMI due to the limited funding pool.6 Taken together, it turned out the NCMS insured IMs had a higher percentage share of OOP payments than the UEBMI/URBMI insured peers. To increase portability of the NCMS, in 2015, China started to develop a national NCMS online reimbursement system so the NCMS enrollees will receive reimbursements on a real-time basis in designated hospitals across regions in 2020.40 Further empirical evidence on the effectiveness of the new policy will be needed. In addition, raising the funding level should also be considered in the future (eg, from county/city level to provincial level) to overcome the fragmentation of SHI systems, increase portability of SHI and reduce restrictions to claiming benefits. For example, Japan has raised the unit of national health insurance finances from the municipal level to the prefectural level, which promoted the achievement of UHC.41

Strengths and weaknesses of the study

To our best knowledge, this study produced evidence on SHI coverage and its financial protection effects that were unavailable for rural-to-urban IMs, which represent about a fifth of the total population in China. It is worth noting that the main contribution of the findings is to compare the relative degree of financial protection across SHI schemes status, rather than to obtain an absolute measure of financial protection, in terms of the level of protection.

This study has a few limitations. First, the measurement was based on self-reported information rather than on data from health insurance database and hospital information system. Thus, the SHI coverage and medical costs may be either underestimated or overestimated due to bias (ie, recall bias). Second, the 2014 NIMDMS was not specially designed for this study and the data were collected before this study. Thus, the data were imperfect for assessing financial protection among IMs. For example, the financial protection effect of SHI schemes represented a low bound because the 2014 NIMDMS did not collect costs of outpatient and multiple inpatient services during the past 12 months. However, as introduced in the Measures section, financial burdens of medical services among IMs were mainly caused by the latest inpatient service.27 Additionally, due to the limits of available data, some confounding factors, such as health or disease status,42 cannot be controlled. Further monographic research on financial protection effects of SHI among IMs is needed. Third, the sample was limited to IMs between 15 and 59 years old. Therefore, our findings are not generalisable to IMs in all age groups, especially the elders who may have greater healthcare needs than young migrants.

Notwithstanding these limitations, our study provides evidence that rural-to-urban IMs face barriers to accessing SHI in China, and SHI had significant financial protection effects. Although hard to access, SHI schemes at migrants’ current residence had a better protection than the scheme in sending regions. The findings suggest that promoting availability of SHI by qualifying migrants for schemes at their current residence, and improving portability of SHI, would promote financial protection for IMs, and further facilitate achieving UHC in China and other countries that face migration-related obstacles to achieve universal coverage.

References

Footnotes

Handling editor Seye Abimbola

Contributors LL got the access to data from the ‘2014 National Internal Migrant Dynamic Monitoring Survey (NIMDMS)'. WC developed analytical strategy, analysed data and drafted the manuscript. QZ and AMNR participated in critically revising the manuscript. FZ contributed to data analysis. All authors contributed to the data interpretation, manuscript writing and final approval of the manuscript.

Funding The NIMDMS was funded by the National Health and Family Planning Commission of China. The funding agency played no role in data analysis, writing of the manuscript, interpretation of the results or submission for consideration of publication. QZ was supported by the 111 Project, grant number B16031.

Competing interests None declared.

Patient consent Obtained.

Ethics approval This was secondary analysis of publicly available data, and no participant consent forms were required to access this data set. This study was approved by the Ethics Committee of School of Public Health, Sun Yat-Sen University.

Provenance and peer review Not commissioned; externally peer reviewed.

Data sharing statement The data controller of the data analysed is the National Health and Family Planning Commission of China. The 2014 NIMDMS data are available subject to authorised researchers who have been permitted by the National Health and Family Planning Commission of China.